Every day I read some sort of wrongheaded extrapolation about the future of AI — that today’s models are somehow indicative of AGI creating a “permanent underclass” of people that stops people from building software companies, or really doing any kind of job on the computer:

Show full content

Every day I read some sort of wrongheaded extrapolation about the future of AI — that today’s models are somehow indicative of AGI creating a “permanent underclass” of people that stops people from building software companies, or really doing any kind of job on the computer:

Hyperbolic? Perhaps. But even those who view the idea of a permanent underclass as overblown tell me that the meme contains a kernel of truth. Yash Kadadi, a 23-year-old start-up founder and Stanford dropout, summarized the sentiment of his peers: “There’s only a matter of time before GPT-7 comes out and eats all software and you can no longer build a software company. Or the best version of Tesla Optimus comes out,” and can perform all physical labor as well. In that world, this year is a human’s “last chance to be a part of the innovation.”

Yash, your peers are fucking idiots. You may as well be talking about breeding Grinches or Ninja Turtles, or kvetching about the upcoming threat from Godzilla. “The best version of Tesla’s Optimus [robot]” suggests that Tesla has released an Optimus robot, or that any prototypes are capable of anything approaching useful work, something that Tesla itself has said isn’t the case.

Every discussion of AI has become a discussion of anywhere between one and a million different theoreticals.

The Information’s headline that OpenAI will “save $97 billion through 2030 in latest Microsoft deal” — one that capped its revenue share (as in the actual money it sends to Microsoft) at $38 billion — hinges on the idea that OpenAI would somehow make $190 billion in revenue, because that’s what it would take to actually max out its revenue share.

The majority of articles about METR’s “time horizon” study of how long models take to complete tasks gush with mindless praise, but regularly leave out two valuable details: that these comparisons are made based on estimates of both human task times, and that the most-commonly shared task is based on how likely it is to complete a task 50% of the time:

The task-completion time horizon is the task duration (measured by human expert completion time) at which an AI agent is predicted to succeed with a given level of reliability. For example, the 50%-time horizon is the duration at which an agent is predicted to succeed half the time.

It’s the Sex Panther joke from Anchorman, except it’s a chart that gets written up in major newspapers and bandied about as proof of models becoming conscious.

Nevertheless, everybody appears to be having a lot of fun making stuff up or making ridiculous assertions based on OpenAI or Anthropic’s predictions. Likely gas leak victim Joseph Jacks posted last week that at its current rate of growth, Anthropic would pass Google’s revenue by 2028. Multiple different people I’d rather not link to are posting benchmarks of Anthropic’s still-to-be-released Mythos model as proof that we’re in the early-to-middle stages of the entirely-fictional AI 2027 “simulation,” despite the entirety of this ridiculous, oafish extrapolation relying on the idea that at some point LLMs become conscious and start doing their own research.

None of these people seem to want to engage with reality, even in their extrapolations.

But what I haven’t done recently — not since AI Bubble 2027, at least — is try my own hand at extrapolating the future based on the things I have read, seen and reported on.

I’ll be honest that there are a lot of unanswered questions I have about the AI bubble that make precise, time-based predictions almost impossible. We’re in the midst of one of the most insane market rallies in history driven around the exploding valuation of NVIDIA and data center related stocks despite there being a great deal of compelling evidence that millions of Blackwell GPUs are sitting in warehouses, meaning that the market is rallying around the idea of data centers getting built without ever confirming whether that’s actually true.

In the past, I’ve approached things from an investigative perspective, proving what I believe to be one of the greatest misallocations of capital in history. Today, I’m going to have a little more fun, exploring both the worrying signs I see and their potential consequences in the form of questions, mixing my own reporting with a little bit of fiction.

Even if Anthropic were able to mop up some of that fallow capacity, it too relies on endless venture capital and hyperscaler welfare to pay, well, increasingly-large shares of hyperscaler revenue.

I feel as if many people are willing to ask if we’re in an AI bubble, but few seem to want to talk about what might happen. It’s really easy to say “stocks are overvalued” or “OpenAI is deeply unprofitable,” but thinking much harder than that starts to make you feel a little crazy.Data center construction now makes up a larger chunk of all construction spending than commercial real estate. OpenAI has made promises that total over a trillion dollars, and Anthropic $330 billion. NVIDIA represents 8% of the value of the S&P 500, and that valuation is based on the idea that it will never, ever stop growing, which is only possible if data center construction never stops. CoreWeave, IREN, Nebius, and Nscale all rely on hyperscaler contracts that are related to OpenAI, and if those contracts go away because OpenAI does, they’re screwed.

Most people can say that these things are true, but very few of them are willing to think about their consequences, because when you do so, things begin feeling completely and utterly fucking insane.

The AI bubble is supported almost entirely by magical thinking and people ignoring obvious warning signs again and again and again in the hopes that at some point something changes. You can quote whatever story you like about Anthropic’s skyrocketing revenues (which are absolutely inflated) — there’s no getting away from the fact that it loses billions of dollars year, and if your answer is that it will turn profitable in 2028, please tell me how because there is no proof that it’s possible.

I also kind of get why nobody wants to think about this stuff. Even though it’s become blatantly obvious that the economics don’t make sense, the stock market continues to rip based on equities connected to the AI bubble in a way that defies logic but rewards positive speculation. Major media outlets continue publishing positive stories about the power of AI that seem entirely-disconnected from what AI can do, and millions of dollars are being spent by companies based on a theoretical return on investment.

“I am preparing myself to be surprised” by the bills, he said. “We believe that there’s a lot of value here. Unfortunately, it’s fairly new technology, so there’s some open questions that we’re gonna be working through” around its costs and getting a return on the investment.

We are fucking years into this man, how is the question of return on investment still an open question?

People also don’t really like thinking about bad things happening. They’re happy to make vague leaps in a direction that makes them feel prepared for the worst (such as the specious statements about all of these data centers being for the military or a theoretical bailout), especially if it makes them feel smart, but in doing so they get to avoid the actual bad stuff — the economic ramifications for ordinary people, the years of depression ahead for the tech industry, and the calamitous results for the market.

So, today, I’m going to have a little fun thinking about the actual consequences of everything I’ve been writing. I’m going to thread in both my own and others’ reporting, and take these ideas to their logical endpoints as far as I can.

This is going to be the first of a two-part exploration of what the actual consequences of the AI bubble bursting might be.

I’ll also caveat this by saying that these are, ultimately, explorations of potential future events rather than cast-iron guarantees. People seem to be resistant to being told the truth, so perhaps it’s time to explore these ideas as theoretical — fictional, even — so that people are more willing to take them in.

This series is all about simple scenarios, and one very simple question.

If you liked this piece, please subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI&

Subscribing to premium is both great value and makes it possible to write these large, deeply-researched free pieces every week.

During every bubble there’s one very obvious thing that keeps happening: things are said, these things are repeated, and are then considered fact. Sam Bankman-Fried was the smiling, friendly, “self-made billionaire” face of the crypto industry. NFTs were the future of art, and would change the way people think about the ownership of digital media.

Three months before his arrest, a CNBC reporter would fly to the Bahamas to hear SBF tell the story of how he “survived the market wreckage and still expanded his empire,” with the answer being that he had “stashed away ample cash, kept overhead low, and avoided lending,” as opposed to the truth, which was “crime.”

The point is that before every scandal is somebody emphatically telling you that everything’s fine. Everything seems real because there’s enough proof, with “enough proof” being a convincing-enough person saying that “most of FTX’s volume comes from customers trading at least $100,000 per day,” when the actual volume was manipulated by FTX itself, and the “$100,000 a day in customer funds” were being used by FTX to prop up its flailing token.

In the end, the “proof” that SBF was rich and that FTX was solvent was that nobody had run out of money and that nothing bad had happened to anybody. SBF was a billionaire sixteen times over because enough people had said that it was true.

Anyway, one of the most commonly-held parts of the AI bubble is that massive amounts — gigawatts’ worth — of data centers have both already been and continue to be built…

Remember, Colossus-1 is an odd data center, with around 200,000 H100 and H200 GPUs and an indeterminate amount of Blackwell GB200s, weighing in at around 300MW of total capacity…which isn’t really that much if we’re talking about gigawatts being built every quarter, is it?

So, I have two very simple questions to ask: how long does it take to build a data center, and how much data center capacity is actually coming online?

These simple questions are surprisingly difficult to answer. There exists very little reliable information about in-progress data centers, and what information exists is continually muddied by terrible reporting — claiming that incomplete projects are “operational” because some parts of them have turned on, for example — and a lack of any investor demand for the truth. Hyperscalers do not disclose how many data centers they’ve built, nor do they disclose how much capacity they have available.

So I went and looked, and what I found was confusing.

Defining “Built” and “Operational”

So, you’re going to hear people say “well Ed, data centers are being built,” and what I’m talking about is data centers that have been fully constructed and then turned on. It’s really, really easy to find data centers that are under construction, but as I’ve discussed in the past, that can mean everything from a pile of scaffolding to a near-complete data center.

Yet finding the latter is very, very difficult. I’ve spent the last week searching for data centers that broke ground in 2023 or 2024 that have actually been finished, and come up surprisingly empty-handed. Some projects are stuck in construction hell, eternally dueling with planning departments over permitting, some are chugging along with no real substantive updates, some, as is the case with Nscale’s Loughton, England data center, have done effectively nothing for the best part of a year, some are perennially adding more capacity to the order as a means of continuing raking in construction bills, and some are claiming their data centers are “operational” as only a single phase has turned on.

You should also know that even once construction has finished, the buildings themselves must be fully filled with the necessary cooling, power and compute hardware, at which point it can be configured to meet a client’s specifications (which can take months), at which point the unfortunate soul building the facility can actually start making money.

Building A Data Center Is Difficult, And Nobody Has Built A 1GW Data Center Yet

I think it’s also worth revisiting how difficult data center construction is, and how large these new projects are.

It’s fundamentally insane how many different companies are trying to build these things considering how difficult even the simplest data center is to build.

Take, for example, American Tower Corporation’s edge data center in Raleigh, North Carolina, which I’ll mention a little later. This is a 1MW facility — or one-thousandth the size of a gigawatt facility — occupying 4000 sq ft of real estate at first and expanding to 16,000 if ATC actually gets it up to 4MW. That’s about two-and-a-bit times larger than the typical American home. And, from ground-breaking to ribbon-cutting, it took eleven months to complete. And that’s not including all the other necessary time-consuming bits, like finding land, securing permits, and so on.

That’s a simple one. People want to build data center campuses a thousand times larger than that. Look at how difficult it is.

In fact, it’s so difficult that the companies can’t build all of it at once. Larger data center campuses are almost always divided into “phases,” in part because that’s the smartest way to build them, and in part with the express intention of convincing you that they’re “fully operational.”

For example, CNBC’s MacKenzie Sigalos reported in October 2025 that Amazon’s Indiana-based (allegedly) 2.2GW Project Rainier data center was “operational,” but only seven out of a planned 30 buildings were actually operational, and her comment of “with two more campuses [of indeterminate capacity] underway.” This comment was buried two videos and 600 words into a piece that declared the data center was “now operational,” with the express intent of making you think the whole thing was operational.

To give her credit, at least she didn’t copy-paste the outright lie from Amazon, which claimed that Rainier was “fully operational” in a press release the same day. You’ll also note that Amazon never provides any clarity about the actual capacity of Rainier.

Sigalos did exactly the same thing when the first (of eight) buildings of Stargate Abilene opened, declaring that “OpenAI’s first data center in $500 billion Stargate project is open in Texas,” burying the comment that only one was operational with another nearly complete several hundred words earlier.

These are intentionally attempts to obfuscate the actual progress of the data center buildout, and if I’m honest, I’ve spent months trying to work out why big companies that were supposedly building large swaths of data centers would be trying to do so.

Unless, of course, things weren’t going to plan.

Is Microsoft Misleading Us About Its Data Center Capacity?

Microsoft claims to have brought around 4GW of data center capacity online in the last two years, but it’s unclear how much actually got built.

In an analysis of all announced groundbreakings and land acquisitions, it appears that Microsoft has only finished the first phase of its Atlanta and Wisconsin data centers.

It is unclear where this capacity could be.

Microsoft Promised Then Failed To Deliver Comment On Its Data Center Capacity

In its last (Q3 FY26) quarterly earnings call, Microsoft CEO Satya Nadella claimed that “[Microsoft] added another gigawatt of capacity this quarter, and [remained] on track to double [its] overall footprint in two years.” A quarter earlier, he claimed to have added “nearly one gigawatt of total capacity,” with Karl Keirstead of UBS saying that he “...thought the one gigawatt added in the December quarter was extraordinary and hints that the capacity adds are accelerating.”

As I’ll discuss below, I can find no evidence of anything more than a few hundred megawatts of Microsoft’s data center capacity coming online. While I’ll humour the idea that it doesn’t announce every new data center, and that there may be colocation and neocloud counterparties (67% of CoreWeave’s revenue comes from Microsoft, for example) that make up the capacity, as I’ll also discuss, I don’t know where the hell that might be.

So, to be aggressively fair, I asked Microsoft to answer the following questions on May 4, 2026:

When Mr. Nadella said on his most-recent earnings call that Microsoft had (and I quote) "added another gigawatt of capacity this quarter," did he mean active, revenue-generating capacity?

In the event he did not, what did he mean?

How much active, revenue-generating capacity has Microsoft brought online in FY2026 so far?

Outside of Fairwater Wisconsin and Atlanta, where has that capacity been built?

A Microsoft representative from WE Communications promised to "circle back" by 5PM ET on Monday May 4th, but did not return further requests for comment via text and email, which is incredibly strange considering the simple and straightforward nature of my questions.

That’s probably because the vast majority of its publicly-announced or documented data center capacity doesn’t appear to be getting finished.

Microsoft Says Its Fairwater Data Centers Are Operational — They’re Actually Unfinished

In September 2025, CEO Satya Nadella claimed that Microsoft had added 2GW of capacity “in the last year,” and acted as if Fairwater, a project with two actively-constructed data centers with one in Wisconsin that broke ground in September 2023 and another in Atlanta that broke ground in July 2024, was something to be “announced” rather than “a very expensive project that has taken forever.” Nadella also claimed that there are “multiple identical Fairwater datacenters under construction,“ though he neglected to name them.

To be clear, “Fairwater” refers to a project where multiple data centers are linked with high-speed networking to make one larger cluster, a project that sounds ambitious because it is, and also unlikely because it’s yet to have been built.

I have serious doubts that Microsoft stood up a 350MW data center in less than a year, given everything else I’m about to explain.

Fairwater Wisconsin is also a data center of indeterminate size, but Cleanview claims Phase 1 is 400MW, quoting a story from FOX6 News Milwaukee from September 2025 that said that Microsoft was “investing an additional $4 billion to expand the campus,” featuring a video of a very much in construction data center saying the following:

Microsoft is in the final phases of building Fairwater, the world’s most powerful AI data center, in Mount Pleasant. Microsoft is on track to complete construction and bring this AI data center online in early 2026, fulfilling their initial $3.3 billion investment pledge.

So, $3.3 billion — at a rate of around $14 million per megawatt per analyst Jerome Darling of TD Cowen — is about 235MW of capacity, which is a lot lower than 400MW.

Seven months later, Satya Nadella said that the Fairwater datacenter in Wisconsin was “going live, ahead of schedule,” a sentence written in the present tense, but also said that it “will bring together hundreds of thousands of GB200s in a single seamless cluster,” which is in the future tense.

It’s a great time to remind you that Microsoft claims that it brought online roughly eight times that capacity (around 2GW) in the past six months.

To make matters worse, it doesn’t appear that Fairwater Wisconsin is actually operational. Ricardo Torres of the Milwaukee Journal-Sentinel reports that Microsoft has said it isn’t actually online, and that while there “...is equipment inside the data center conducting start-up opportunities…the company anticipates [they] will continue to happen for the next several weeks.”

Epoch AI’s satellite footage of Fairwater Wisconsin — which mentions a completely wrong capacity because it’s uniquely terrible at calculating it (it claimed Colossus-1 has 425MW capacity, for example) — notes that as of April 2026, one building appeared to be operational, with a second under construction.

In simpler terms, there’s at most around 117MW of capacity running at Fairwater Wisconsin.

Sidenote: To be clear, I think some revenue is being generated from a Fairwater data center, as my reporting from last year on OpenAI’s inference spend involved a few million dollars’ worth of billing for “Fairwater,” but it’s unclear whether that referred to Fairwater Atlanta or Wisconsin.

Epoch AI’s satellite footage notes that as of February 2026, building four’s roof was complete and “all mechanical equipment appears to be installed,” but “there is still a lot of construction activity around the building.” Based on air permits filed as part of the project (that Epoch found), it appears that each building is powered by a number of Caterpillar 3516C Generator Sets at around 2.5MW each, with building one having 47 (117.5MW), building two having 13 (32.5MW), building three having 30 (75MW), and building four having 35 (87.5MW).

If we’re very generous and assume that three buildings are complete, that means that Fairwater Atlanta is at around 225MW of capacity (not IT load!).

So, that’s about 342MW of data center capacity being built by one of the largest companies in the world, in its most-publicized and written-about data centers.

Put another way, for Microsoft to come remotely close to its so-called 2GW of capacity in the last six months, it will have had to bring online a little under six times that capacity.

I’m calling bullshit.

None of Microsoft’s Announced Data Center Capacity Since 2024 Has Been Completed

I really did want Microsoft to give me some answers, but I’m very confused as to how it can remotely claim it brought even a gigawatt of capacity online in the last year.

I also question whether Microsoft is actually building multiple other “identical” Fairwater data centers, as I can’t find any announcements or pronouncements or mentions or hints as to where they might be.

In fact, I’m having a little trouble finding where else Microsoft has been building data centers, and those I can find are extremely suspicious.

For two straight quarters, Microsoft has said it’s brought on an entire gigwatt of capacity,and I have to ask: where?

Because when you actually look at the projects it’s announced, very little appears to have been built, and that which has is nowhere near its theoretical capacity.

To be specific about what Microsoft is claiming, it’s saying it’s brought around 4GW of capacity online in the space of two years, and at a 1.35 PUE, that’s about 2.96GW of critical IT load, which works out to the power equivalent of around 284,600 H100 GPUs, which may be possible — after all, Microsoft apparently bought 450,000 H100 GPUs in 2024 — but I can’t find much evidence of data centers that could house that many GPUs, nor that might be in construction.

Microsoft’s latest update on the Hickory/Stover site is that it “will” begin “initial site setup and earthwork activities” as of February 2026, and it appears the contractor has changed from Ames Construction to Clayco.

The latest Microsoft update on the Lyle Creek site — which it adds began construction in March 2024 — is that its contractor, Whiting-Turner, “will begin initial site preparation once weather conditions allow” as of February 2026.

Okay, well, maybe it’s a Canada problem. What about Microsoft’s New Albany, Ohio data center that broke ground in October 2024? Well, as of March 2026, “spring activity would resume,” and “beginning soon, soil will be delivered to the site via a designated truck route. I’ll note that Microsoft specifically says that Ames Construction is currently leading it, and that it will “resume the lead role in project communications” once the final phase of construction is done at some unknown time.

Alright, well, how about the August 2025 ground breaking in Cheyenne, Wyoming that was allegedly “due to launch in 2026”?

Well, Microsoft hasn’t updated its community page since it said there’d be a community meeting planned for November 2025 and that “neighbors within the vicinity will be notified ahead of construction,” which sounds like construction is yet to commence. Not to worry though, it announced on April 14, 2026 that it planned to expand it to “accelerate innovation and economic growth”

This company claims it’s built four fucking gigawatts of capacity, but when I go and look to see what it’s actually built I’ve failed to find a single announced data center from the last three years that got turned on outside of its Fairwater Atlanta and Wisconsin sites.

To be clear, all of these sites are somewhere in the 200MW to 300MW range. For Microsoft to have brought online 4000MW of data center capacity in the last two years would require it to have completed thirteen or more of these projects, all while choosing not to promote them, with every project operating in such a veil of secrecy that no local or national news outlet reported a single one of them.

I truly cannot work out how Microsoft has brought on any more than 500MW of capacity in the last year based on my research, and think Microsoft is deliberately obfuscating whether said capacity was contracted rather than actively in-use, much like CoreWeave refers to itself having 3.1GW of “total contracted power” but only added 260MW of active power capacity in a single quarter at the end of 2025.

Sidenote: If you’re wondering why CoreWeave didn’t include how much active power it added in its Q1 2026 earnings press release, it’s because (per its own earnings presentation) it only added 150MW, in a quarter it contracted 400MW. It also said it added six new data centers, which I doubt.

However, the exact verbiage used in Microsoft’s earnings transcripts is that it “added another gigawatt of capacity,” which sounds far more like it’s saying it brought them online…

…but it didn’t, right? It obviously hasn’t.

Where are all the data centers, Satya? Where are they? Why are your PR people too scared to tell me?

No, really, where are they?

So, to be fair, analyst Ben Bajarin, one of the more friendly pro-AI posters, argues that actually all of that capacity is secretly behind-the-scenes, something I’d humour if there was any kind of paper trail to a bunch of Microsoft data centers that were secretly being built.

I’d also be more willing to humour it if any of the data centers that have been publicized as “breaking ground” had actually been finished, or if both Fairwater Atlanta and Wisconsin weren’t so deceptively-marketed.

My only devil’s advocate is that Microsoft could, in theory, be working with colocation partners to stand up several gigawatts of capacity through shell corporations and SPVs, but even then, not a single one has any sort of trail to Microsoft? All of that capacity?

It’s really, really weird, and the only answers I get are smug statements about how “Fairwater is ahead of schedule.”

But if I’m honest, I’m having trouble even making these numbers add up.

No, Really, Where Are All The Data Centers?

Considering how loud, offensive and conspicuous the AI bubble has become, it feels like we should have a far, far better understanding of how much actual capacity has been built.

I also think it’s time to start being realistic about how long these things are taking to build.

For example, I was only able to find a few data centers that for sure, categorically, definitively opened, and for the most part, it appears that a data center takes around 18 months to go from groundbreaking to opening.

And these, I add, are all facilities that are relatively modest — at least, when compared to the kinds of gigawatt-scale campuses that are reportedly in active development.

Novva’s 60MW data center in Reno, Nevada. Announced in May 2023, operational as of July 2025, or around 26 months.

EdgeCore’s 36MW Santa Clara, California data center campus that broke ground in January 2023, said it would be “energized in Q1 2024,” and opened in September 2025, or around 32 months.

Digging deeper, I found a lot of projects stuck in development Hell:

PowerHouse’s 65MW data center campus in Reno, Nevada broke ground in October 2024, and its website states that “delivery” will happen in April 2026, with “construction/delivery” due “Q3 2024 to Q2 2026.”

Oppidan’s Carol Stream, Illinois data center broke ground in November 2024, with the “first phase” due live in 2026. Per Clearview, it is still “planned.”

Flexennial, on the other hand, has been referring to it as “the new build” — in terms that make it sound like it was built — as far back as February 2025.

While there are absolutely data centers under construction, and some, somewhere, are actually being completed, the vast majority of projects I’ve found are either in a mysterious limbo state or, in most cases, under construction years after breaking ground.

Across the board, the message seems to be fairly simple: it takes about 18 to 24 months to build any kind of data center, and the bigger they are, the less likely they are to get completed on schedule.

Those that actually “come online” aren’t actually fully constructed, but have brought on a single phase — something I wouldn’t begrudge them if they were anything close to honest about it. In reality, data center companies actively deceive the media and customers about the actual status of projects, most likely because it’s really, really difficult to build a data center.

In any case, what I’ve found amounts to a total mismatch between the so-called “rapid buildout” of AI data centers and reality.

It also doesn’t make much sense when you factor in how many GPUs NVIDIA sold.

I Do Not Believe That More Than One Million Blackwell GPUs Are Actually In Operation — Meaning That Two Million GPUs Are Sitting In Warehouses

In October last year, NVIDIA CEO Jensen Huang told reporters that it had shipped six million Blackwell GPUs in the last four quarters, though it eventually came out that he was counting two cores for every GPU, making the real number three million. I disagree with the framing, I think it’s incoherent and dishonest, but I’ve confirmed this is what NVIDIA meant.

In any case, if we assume two cores per GPU, a B200 GPU has a power draw of around 1200W, for around 3.6GW of IT load for 3 million of them. I realize that NVIDIA also sells B100 and B300 GPUs (similar power draw) and NVL72 racks of 72 GB200 GPUs and 36 CPUs, but bear with me.

Blackwell GPUs only started shipping with any real seriousness in the first quarter of 2025, which means that a good chunk of these data centers were built with H100 and H200 GPUs in mind. Nevertheless, I can find no compelling evidence that significant amounts — anything over 500,000 GPUs — of Blackwell-based data centers have been successfully brought online.

When I say I struggled to find data centers that had been both announced and brought online, I mean that I spent hours looking, hours and hours and hours, and came up short-handed.

I want to be clear that I know that there is Blackwell capacity actually being built, and believe that the majority of that capacity is retrofits of previous data centers, such as Microsoft’s extension to its Goodyear Arizona campus which it began building in 2018 that likely houses Blackwell GPUs.

But I no longer believe that the majority of Blackwell GPUs are doing anything other than collecting dust in a warehouse. Blackwell GPUs require distinct cooling, a great deal more power than an H100, and cost an absolute shit-ton of money, making it unlikely that a 2023 or early-2024 era data center could handle them without significant modifications.

I fundamentally do not believe more than a million — if that! — Blackwell GPUs are actually in service.

If that’s the case, NVIDIA is likely pre-selling GPUs years in advance — experimenting with the dark arts of “bill-and-hold” — and helping certain partners like Microsoft install the latest generation to create the illusion of utility, availability and viability that does not actually exist.

If I’m honest, I also have serious questions about the current status of many H100 and H200 GPUs. Based on what I’ve found, I’d be surprised if more than 3GW of actual capacity was turned on in the last two years, which means that NVIDIA has sold anywhere from double to triple the amount of GPUs that the world can hold.

Data Center Capacity Isn’t Turning On At The Rate We Think, And It’s Choking The AI Industry

While the Anthropic-Musk compute deal is an obvious sign about xAI’s lack of demand for compute, it’s also, as I mentioned earlier, a clear sign that AI data centers are mostly not getting finished, and those that do get finished are taking two or three years even for smaller builds.

While it sounds a little wild, I think in reality only a few hundred megawatts — if that — of actual, usable AI compute capacity is being spun up every quarter. If I was wrong, there’d be significantly more progress on, well, anything I could find.

Why can’t Microsoft offer up a data center that isn’t called Fairwater, and why are its Fairwater data centers taking so long? How much actual capacity has Microsoft brought online? Because it certainly isn’t fucking 2GW in six months.

I’m willing to believe that Microsoft has a number of collocation agreements with parties that don’t disclose their involvement. I’m also willing to believe that Microsoft doesn’t publicize every single data center it’s building or has built.

2GW of capacity is a lot. It’s nearly ten times the (likely) existing capacity of Fairwater Atlanta. If Microsoft is bringing so much capacity online, why can’t we find it, and why won’t they tell us? And no, this isn’t some super secret squirrel “they’re building secret data centers for the government” thing, it’s very clearly a case where “capacity” refers to “something other than data centers that actually got brought online.

It Is Very Unlikely That Gigawatts of Data Center Capacity Are Coming Online Every Quarter

Despite their ubiquity in the media, AI data centers are relatively new concepts that are barely five years old. They are significantly more power-intensive than a regular data center, requiring massive amounts of cooling and access to water to the point that the surrounding infrastructure of said data center is often a massive construction project unto itself.

For example, OpenAI and Oracle’s Stargate Abilene data center is (in theory) made up of two massive electrical substations, a giant gas power plant and eight distinct data center buildings, each with around 50,000 GB200 GPUs, at least in theory. Every data center requires that power exists — as in it’s being generated in both the manner and capacity necessary to turn it on, either through external or grid-based power — and is accessible at the data center site.

This means that every single data center, no matter how big, is its own construction nightmare. You’ve got the power, the labor, the permits, the planning, the construction firm, the power company, the specialist gear, the temporary power (because on-site power is slow), the backup power (because you can’t just rely on the grid for something you’re charging millions for!), the cooling, the uninterruptible power supplies — endless lists of shit that needs to go very well or else the bloody thing won’t work.

Let’s go back to Anthropic mopping up Musk’s fallow data center capacity, which stinks of desperation for both companies. If there were modern data centers full of GB200s being turned on and available anywhere in the next month or two, wouldn’t it be more financially prudent to wait for it, even if it’s just on an efficiency level? A franken-center made up of H100s and H200s with some GB200s stapled onto the side feels like a stopgap solution.

It’s also important to remember that last year, OpenAI’s margins (which are already non-GAAP), per The Information, were worse than expected because (and I quote) it had to “..to buy more expensive compute at the last minute in response to higher than expected demand for its chatbots and models.”

Surely you’d wait a few months for some new, less tainted source of compute, right? And surely it wouldn’t be such a big deal, because new data centers get switched on every day, right?

Right?

If Data Centers Aren’t Getting Built, Everything About The AI Bubble Breaks

Look, I know it sounds crazy, but I’m telling you: I don’t think very many data centers are coming online! While I keep wanting to hedge my bets and say “I bet a few gigawatts came online,” I cannot actually find any compelling literature that backs up that statement. I’ve spent hours and hours looking, and I’ve come up with a few hundred megawatts delivered in the past two years. Every major project is stuck in the mud, a phase or two in, or facing mounting opposition from locals that don’t want a Godzilla-sized cube making a constant screaming sound 24/7 so that somebody can generate increasingly-bustier Garfields.

I’m not even being a hater! It’s just genuinely difficult to find actual data centers that have been announced that have also been fully turned on.

That $800 Billion In Capex Is Yet To Truly Enter Depreciation

So, humour me for a second: if hyperscalers are bringing on hundreds of megawatts of capacity a year, then that means that the ever-growing quarterly chunks of depreciation ripped out of their net income are just a taste of what’s to come.

Last quarter, Google’s depreciation jumped $400 million to $6.482 billion, with Microsoft’s jumping nearly a billion dollars from $9.198 billion to $10.167 billion, and Meta’s from $5.41 billion to $5.99 billion. While Amazon’s technically dropped quarter-over-quarter, it still sat at an astonishing $18.94 billion.

Remember: depreciation only increases when an item is actually put into service. If Microsoft, Google, Amazon and Meta are sitting on tens of billions of yet-to-be-installed GPUs, and said GPUs are only being installed at a snail’s pace every quarter, that means that these depreciation figures are set to grow dramatically. In fact, year-over-year, Google’s depreciation has jumped 30.7%, Amazon’s 24.7%, Microsoft’s 23.9%, and Meta’s an astonishing 34.9%.

And that’s with an extremely slow pace of deployment.

Sidenote: This also really makes me doubt that Microsoft has been bringing a gigawatt of GPU capacity for two quarters straight. A gigawatt of GPU capacity would be about $2 billion a quarter or more in depreciation. A $400 million bump in depreciation is about $9.6bn ($400 million times 24 quarters (6 years)), at about $50,000 per B200 GPU, or around 192,000 GPUs at 1200W each, for around 230.4MW.

Hell, someone could probably sit down and work out their potential capacity based on depreciation alone.

I do kind of see why the hyperscalers are sinking capex into these big AI infrastructure gigaprojects now, though. Shareholders are currently tolerating the capex because they think stuff is coming online, and that’s where the “incredible value” is. When a $20 billion or $30 billion a quarter depreciation bill first rears its head — as I said, Amazon is close, reporting $18.945bn in depreciation and amortization expenses in the most recent quarter — it’ll become obvious that the only people seeing value from AI are Jensen Huang and one of the massive construction firms slowly building these projects.

Actually, it’s probably important to state that I don’t think the majority of these projects are doing anything untoward I just don’t think any of them realized how difficult it is to build a data center, and unlike basically any other problem the tech industry has ever faced, simply throwing as much money as possible at it doesn’t really change the limits of physical construction.

I think every one of these data center projects is its own individual construction nightmare, and thanks to the general market psychosis around the AI bubble, nobody has thought to question the core assumption that these things are actually getting built.

With all that being said, I’m not sure that anyone building these things is moving with much urgency either. Perhaps they don’t need to — perhaps hyperscalers are happy, because they can continually string out both the AI narrative and put off those massive blobs of depreciation.

Maybe they can really pick up the pace, but as of early April, barely any actual gear was in the third building.

And then we get to the other problem: Oracle.

The Slow Pace of Data Center Development Is Lethal To Oracle, OpenAI, and Anthropic

As I’ve discussed before, Oracle is building 7.1GW of total capacity for OpenAI, and keeps — laughably! — saying 2027 or 2028, when at this rate, Stargate Abilene won’t be done until mid-2027, and the rest either never get finished or are done in 2030 or later.

This is setting up a horrifying situation where Oracle desperately needs OpenAI to pay it for capacity that doesn’t exist, and if it ever gets built, it’s likely to be years after OpenAI has run out of money, which is the same problem that Microsoft, Google, and Amazon have with their $748 billion of deals with Anthropic and OpenAI, though thanks to the $340 billion or more necessary to build the Stargate data centers, Oracle’s problems are far more existential.

I’ve repeatedly — and correctly! — said that the problem is that these companies didn’t have the money to pay for their capacity, but Oracle lacks Microsoft or Google’s existing profitable businesses to fall back on if these data centers are delayed, with its existing business lines plateauing and its only real growth coming from theoretical deals with OpenAI and GPU compute with negative 100% margins.

Anthropic’s desperation for new sources of compute also suggests that it’s bonking its head against the limits of its capacity, and will continue to do so as long as it continues to subsidize its users. I also think that the slow pace of construction will eventually lead to OpenAI facing similar problems.

These companies need to continue growing to continue to raise the hundreds of billions of dollars in funding necessary to pay Oracle, Google, Microsoft, and Amazon their respective pounds of flesh.

It’s now very clear that the whole “inference is profitable” and “most compute is being used for training” myths are dead, because if they weren’t, Anthropic would either need way more compute or way higher-quality compute. Colossus-1 was specifically built as a training cluster, yet its current use is “reduce rate limits for our subsidized AI subscriptions,” which is most decidedly inference provided by three-year-old hardware.

What If Only A Gigawatt Of Capacity Is Coming Online Every Year? Every Data Center Takes 18-24 Months+ To Build

Despite writing over 9000 words and driving myself slightly insane trying to find out, I still haven’t got an answer as to how much actual data center capacity has come online. Hyperscalers have clearly been retrofitting old data centers to fit their new chips, and based on my research, I can find no compelling evidence that they’ve added more than a few hundred megawatts a piece since 2023.

What I do know is that, across the board, a data center of anything above 50MW (or lower, in some cases) takes anywhere from 18 to 36 months to complete, and nobody has actually built a gigawatt data center despite how many people discuss them.

For example, Kevin O’Leary — known as “Mr. Dogshit” to his friends — is allegedly building a 9GW data center in Utah, but he may as well say that he’s building a unicorn that shits Toyota Tacomas, as doing so is far more realistic than a project that will likely cost $396 billion, assuming that locals and bankers don’t drag him to The Other Side like Dr. Facilier.

Nobody has built a 1GW data center, so I severely doubt Mr. Dogshit will be able to do anything other than create another scandal and lose a bunch of people’s money.

In other words, any time you hear about a “new data center project,” add a year or two to whatever projection they give. If it’s 2027, assume 2029, or that it never gets built. Anything being discussed as “finished in 2030” may as well not exist.

Sidenote: In general, the only projects that take anything less than a year are tiny — a megawatt max — other than Elon Musk’s Colossus-1, a Frankenstein’s monster of GPUs that vary between 1 and 3 years old.

In any case, what I’m suggesting is that very, very few data centers are actually getting finished, and if that’s true, NVIDIA has sold years worth of chips that are yet to be digested.

And if that’s true, somebody is sitting on piles of them.

I’m trying to be fair, so I’ll assume that an unknown amount of data centers got retrofitted to fit Blackwell GPUs. But I also refuse to believe that even half of the three million Blackwell GPUs that got shipped have actually been installed. Where would they go? You can’t use the same racks for them that you would with an H100 or H200, because Blackwell requires so much god damn cooling.

Why not? Isn’t this meant to be a chip that’s extremely valuable? Isn’t there infinite demand? Is there not a place to put them? Apparently Oracle wanted to use faster GB200 GPUs from Dell, but why aren’t there other customers lining up to buy these things?

Also…how was Oracle able to cancel an order of over a billion dollars’ worth of GPUs?

Can anybody do that? Because if they can, one has to wonder if this doesn’t start happening as people realize these data centers aren’t getting built.

The Data Center Construction Crisis Is Only Beginning

Pick a data center. It’s probably barely under construction, or if it’s “finished” it’s actually “partly done” with no real guide as to when the rest will finish.

That data center is a major reason that people value Nebius’ stock! It cannot make a dollar of revenue without its existence! It has the funds and blessing of Redmond’s finest — the Mandate of Heaven! — and it can’t get things done! This is bad, and indicative of a larger problem in the industry — that it’s really difficult to build data centers, and for the most part, they’re not being fully built!

You’ve heard plenty about data centers getting opposed and canceled — how about ones that fully opened? No, really, if you’ve heard about them please get in touch, because it’s really difficult to find them.

Why don’t we know? This is apparently the single most important technology movement since whatever the last justification somebody made up was, shouldn’t we have a tangible grasp? Because the way I see it, if these things aren’t coming online at the rate that people think, we have to start asking for fundamental clarity from NVIDIA about where the GPUs are, and when they’re coming online.

NVIDIA’s continually-growing valuation is based on the conceit that there is always more demand for GPUs, and perhaps that’s true, but if this demand is based on functionally selling chips two years in advance. That makes NVIDIA’s yearly upgrade cadence utterly deranged. Buy today’s GPUs! They’re the best, for now, at least. By the time you plug them in they’re gonna be old and nasty. But don’t worry, it’ll take two years for you to install the next one too!

To be clear, Blackwell GPUs are absolutely being installed! But three million of them?

People love to use “enough to power two cities” to illustrate these points, but I actually think it’s better to illustrate in real data center terms.

Stargate Abilene has taken two years to build two buildings of around 103MW of critical IT load. 3 million B200 GPUs works out to about 3.6GW of IT load. Do you really think that nearly thirty five Stargate Abilene-scale buildings were built in 2025? If so, where are they, exactly?

You may argue that other data centers are smaller, and thus it would be easier to build. So why can’t I find any examples of where they’ve done so?

By all means prove me wrong! It’s so easy! Just show me a data center announced or that broke ground in 2023 and find obvious proof it turned on. I’ll even give you credit if it’s partially open!

The problem is that I keep finding examples of “partially complete” and those are the only examples of “finished” data centers.

Isn’t this a little insane? This is all we’ve heard about for years, everybody is ACTING like these things exist at a scale that I’m not sure is actually true!

I expect a fair amount of huffing and “well of course they’re coming online” from the peanut gallery, but come on guys, isn’t this all kind of weird? Even if you want to marry Sandisk and name your children “Western” and “Digital,” why can’t you say with your whole chest several data centers that got finished? We have macro level “proof” but when you try and look at even a shred of the micro you find a bunch of guys with their hands on their hips saying “sorry mate that’ll be another $4 million.”

Something doesn’t line up, and it’s exactly the kind of misalignment that happens in a bubble — when infrastructural reality disconnects from the financials. NVIDIA is making hundreds of billions of dollars and it’s unclear how much of it is from GPUs installed in operational data centers. It feels like Jensen Huang might have run the largest preorder campaign of all time.

This has massive downstream consequences. Sandisk, Samsung, SK Hynix, Broadcom, AMD, Microsoft, Google, Oracle, and Amazon’s remaining performance obligations total [find] and are dependent on being *able* to sell gigawatts worth of computing gear or compute access. If data centers are not getting built in anything approaching a reasonable timeline, that makes the future of these companies only as viable as the construction projects themselves. Even if you truly believe Anthropic will be a $2 trillion company and a $200 billion customer of Google, the compute capacity has to exist to be bought, and it does not appear to be built or, in many cases, anywhere further than the earliest stages of construction.

If they don’t get built in the next few years, there’s no space for that solid state storage or those instinct GPUs. There’s no reason for NVIDIA to have reserved most of TSMC’s capacity, either.

Anthropic not have money to pay big cloud bills, because Anthropic company cost lots of money, more money than Anthropic make! So Anthropic only PAY cloud bills if OTHERS

Anthropic not have money to pay big cloud bills, because Anthropic company cost lots of money, more money than Anthropic make! So Anthropic only PAY cloud bills if OTHERS give it money! Amazon GIVE MONEY to Anthropic to GIVE BACK TO AMAZON, which mean no profit! And Amazon not give Anthropic enough money to pay it, so Anthropic have to ask OTHERS for money! That BAD! It mean BUSINESS not STABLE, and CLIENT not STABLE.

This bad when client MOST OF AI MONEY!

This ALSO mean that Anthropic RELIANT on OTHERS to pay AMAZON, which make AMAZON dependent on VENTURE CAPITAL for FUTURE REVENUE! Amazon SAY it have BIG BUSINESS, but BIG BUSINESS dependent on ANTHROPIC, which mean BIG BUSINESS dependent on VENTURE CAPITAL!

This SAME for GOOGLE! Both say they have BIG CLIENT, but BIG CLIENT MONEY not supported by REVENUE, so BIG CLIENT actually mean “HOW MUCH VENTURE CAPITAL MONEY ANTHROPIC HAVE.”

This bad business!

Sidenote: Me know you say “ANTHROPIC STOCK WORTH BIG MONEY,” but me need you remember how much capex Amazon and Google spend! Even if Anthropic stake worth $200 Billion, Amazon and Google still spend MANY more dollar than that on capex! And stake so BIG that neither able to SELL ALL. Only make gain on PAPER, which not REAL MONEY!

That’s $748 billion of the entire revenue backlog — not just AI compute — that’s dependent on Anthropic and OpenAI, two companies that cannot afford to pay these bills without constant venture capital infusions from either investors or the hyperscalers themselves.

If xAI doesn’t need 300MW of compute capacity that it spent at least $4 billion to build, who, exactly, are the other large customers for AI compute? I’m not even being facetious. I truly don’t know, I can’t find them, I spent most of last week looking for them, and the only answer I had a week ago was “Elon Musk buying a lot of compute for xAI to make the freaks on the Grok Subreddit able to generate pornography.”

To put this very, very simply: xAI should, in theory, have massive demand for AI compute, but its demand is apparently so small that it can flog a multi-billion-dollar data center to a competitor.

Sightline Climate found that 15.2GW of capacity is under construction and due to be completed by the end of 2027, and at this point I’m not sure anybody can make a compelling argument as to why it’s being built or who it’s for.

Who needs it? Who are the customers? Who is buying AI compute at such a scale that it would warrant so much construction? Where is the demand coming from if it’s not OpenAI and Anthropic?

These questions shouldn’t be that hard to answer, but trust me, I’ve tried and cannot find a GPU compute customer larger than $100 million a year, and honestly, that customer was xAI.

Through many hours of research, I’ve found that the vast majority — as much as 95% — of all compute demand comes from a few places:

Meta, for reasons that defy logic.

Microsoft, for OpenAI’s compute.

Google, for Anthropic’s compute.

Amazon, for Anthropic.

OpenAI.

Anthropic.

Otherwise, every data center deal you’ve ever read about is for a theoretical future customer or an unnamed “anchor tenant” that gives them “guaranteed, pre-committed occupancy” without being identified in any way.

And man, I cannot express how fucking difficult it is to find actual data center customers outside of the ones I’ve named above. In fact, it’s pretty difficult to find any customers for GPU compute not named Anthropic, OpenAI, Microsoft, Google, Meta or Amazon.

90%+ Of All AI Software and Compute Revenues Go Through Anthropic or OpenAI

Outside of OpenAI and Anthropic, effectively no AI software makes more than a few hundred million dollars a year, and to make that money, they have to spend it on tokens generated by models run by one of those two companies.

When those companies generate those tokens, they then flow to one of a few infrastructure providers — I’ll get to the breakdown shortly — to rent out GPUs.

As I’ve discussed this week, at least 75% of Microsoft, Google and Amazon’s AI revenues come from OpenAI or Anthropic, and that’s before you count the money that Microsoft, Google and Amazon make reselling models from both companies.

To get specific, The Information reports that Anthropic will pay around $1.6 billion to Amazon for reselling its models. OpenAI, per my own reporting, sent Microsoft $659 million as part of its revenue share.

AI startups — all of whom are terribly unprofitable — predominantly spend their funding on models sold by OpenAI and Anthropic. Per Newcomer, as of August last year, Cursor was spending 100% of its revenue on Anthropic. Harvey, an AI tool for lawyers, raised $960 million between February 2025 and March 2026, with most of those costs flowing to Anthropic and OpenAI.

Effectively every AI startup is a feeder for API revenue for Anthropic or OpenAI, and as a result, almost every dollar of AI revenue flows to either Google, Microsoft or Amazon.

As Anthropic and OpenAI are extremely unprofitable, Google, Microsoft and Amazon then take that money and either re-invest it in OpenAI and Anthropic, as Google, Amazon and Microsoft have all done in the past few years.

They likely also thought their own services would grow fast enough to warrant the expansion, or that other large GPU consumers would rear their heads.

That never happened. Instead, OpenAI grew bigger and more-demanding of Microsoft’s compute capacity, leading to Microsoft allowing it to seek other partners, in part (per The Information) because some executives believed OpenAI would die:

After striking the blockbuster deal in 2023, several top Microsoft executives told colleagues around that time that they thought OpenAI’s business would eventually fail, even if its technology was good, according to a former manager who discussed it with them.

Meanwhile, Amazon and Google thought they had it made. Anthropic was growing, and its compute demands were reasonable enough that neither had to stretch themselves too thin…until the second quarter of 2025, when Anthropic’s accelerated growth led to it starting to push against the limits of Google and Amazon’s capacity.

So Google agreed to backstop several billion dollars behind twodeals with Fluidstack, a brand new AI compute company, and Amazon continued expanding its Project Rainier data center.

And all of this is only happening because, based on my analysis, very little actual demand for AI compute exists outside of OpenAI and Anthropic, and OpenAI and Anthropic only exist because of Microsoft, Google, and Amazon both building and expanding their infrastructure to cater to them.

In reality, OpenAI and Anthropic are the only meaningful companies in the AI industry. They are the majority of revenue, the majority of capacity and the majority of demand. Microsoft, Google and Amazon have exploited the desperation in a tech industry that’s run out of hypergrowth ideas, and created a near-imaginary industry by propping up both companies.

The mistake that most make in measuring the circularity of OpenAI and Anthropic is to focus entirely on the money raised — $13 billion from Microsoft and up to $50 billion from Amazon for OpenAI, and as much as $80 billion from Amazon and Google for Anthropic.

The correct analysis starts with measuring infrastructure. Based on discussions with sources and analysis of multiple years of reporting, I estimate that of the roughly $700 billion in capex spent by Google, Meta and Microsoft since 2023, at least 5.5GW of capacity costing at least $300 billion has been built entirely for two companies. This has in turn inflated sales through multiple counterparties involving NVIDIA, ODMs like Quanta, Foxconn, Supermicro and Dell, and created a form of market-driven AI psychosis that inspired Meta to burn over $158 billion in three years and the entire world to convince itself that AI was the biggest thing ever.

The reason that there isn’t another OpenAI or Anthropic is that Google, Microsoft, and Amazon bankrolled their entire infrastructure, fed them billions of dollars, and then charged them discount rates for their early compute, with sources telling me that Anthropic pays vastly below-market-rates for Trainium compute from Amazon, and The Information reporting that OpenAI was paying $1.30-per-A100-per hour in 2024, or at or around the cost of running them.

By sacrificing their entire infrastructure to OpenAI and Anthropic, the hyperscalers created the illusion of demand by feeding themselves money, all while buying endless GPUs and TPUs to fill further data centers for two customers, both of whom paid discount rates that lost them money.

This capex bacchanalia gave all three companies a massive boost to their stock prices, so they kept going, even though there wasn’t really demand other than for Anthropic or OpenAI, two companies that they had to constantly cater to with investment capital and server maintenance.

The belief became that all you had to do was plan to build a data center and you’d print money, boosting NVIDIA’s sales and associated counterparties in memory stocks like Sandisk. Except that never happened.

Every data center provider that doesn’t have an Anthropic, OpenAI, or Meta-related contract makes pathetic amounts of revenue that can barely keep up with their debt. AI startups make meager revenues, and lose multitudes more than they can ever hope to make.

The entire AI industry relies upon two companies that expect to burn at least $1 trillion in the next four years, with Anthropic, the supposed “compute-conscious” AI company, committing to at least $330 billion in spend in the next few years.

Where does that money come from, exactly? Because neither of these companies have anything approaching a path to profitability.

Nowhere is this lack of true demand more obvious than in the neoclouds, which only seem capable of signing big deals with Anthropic, OpenAI, Microsoft (for OpenAI), and Google (for OpenAI). Oh, and Meta, who is doing this because the existence of ChatGPT gave Mark Zuckerberg such profound AI psychosis that he’s made Meta build him a CEO chatbot to talk to and burned over $150 billion.

The AI industry is a brittle, circular economy, one only made possible by a lack of financial regulation and a tech industry that’s run out of ideas. Without hyperscalers propping up OpenAI and Anthropic, there would be no reason to buy so many GPUs or build so many data centers, and neoclouds would have no reason to exist.

This is a giant con, a giant illusion, and a giant mistake.

Coming Up On This Week’s Where’s Your Ed At Premium…

90%+ of all AI revenues flow through Anthropic and OpenAI.

90%+ of all AI compute demand comes from Anthropic, OpenAI, Meta, or associated counterparties like Google and Amazon buying compute for Anthropic or OpenAI.

The vast majority of AI operations don’t require more than a few hundred to a thousand GPUs for inference, and at most 20,000 GPUs for training models.

This means that for the 15.2GW of data centers under construction before 2027 ($157 billion in annual revenue) to make sense, thousands of companies will have to rent hundreds or thousands of GPUs.

This also means that the DeepSeek problem — the reason that everybody freaked out in January 2025 — is actually industry-wide.

More than 50% of Microsoft, Google, Amazon, CoreWeave, and Oracle’s entire revenue backlogs are from OpenAI and Anthropic.

Neoclouds are unsustainable, imaginary businesses only made possible by continual subsidies from NVIDIA and the compute demands of OpenAI, Anthropic and Meta.

Outside of Anthropic and OpenAI, only around $13 billion in AI compute demand exists, with much of it taken up by Meta and NVIDIA backstopping neoclouds like CoreWeave and IREN.

ODMs like Supermicro, Dell, Quanta and Foxconn are largely dependent on AI server revenues that largely flow through OpenAI and Anthropic’s counterparties to fuel their server demand.

If you liked this piece, please subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI&

Show full content

If you liked this piece, please subscribe to my premium newsletter. It’s $70 a year, or $7 a month, and in return you get a weekly newsletter that’s usually anywhere from 5,000 to 18,000 words, including vast, detailed analyses of NVIDIA, Anthropic and OpenAI’s finances, and the AI bubble writ large.

Subscribing to premium is both great value and makes it possible to write these large, deeply-researched free pieces every week.

God, it’s been a long few years, and only feels longer after every ecstatic, ridiculous round of tech earnings where the world’s largest companies do everything they can to obfuscate the ugly truth behind their numbers.

By the end of 2027, big tech will have sunk $2 trillion into AI capex, with very little to show for it.

Oh, I know what you’re going to say. “These companies are growing faster than ever!” “These companies are building for future revenue streams!” “These companies are saying that AI is driving growth!”

Yet those revenues are, in the case of Meta and Google, not good enough to actually share.

While Google CEO Sundar Pichai will gladly say that “[Google’s] AI investments and full stack approach are lighting up every part of the business,” said “lighting up” never results in a revenue number that you can point at, because Google knows that analysts and journalists will read “Gemini Enterprise has great momentum with 40% quarter on quarter growth” — which we have no frame of reference for because Google doesn’t share its AI revenues — and clap and honk like fucking seals. Sundar Pichai knows that everybody is desperate to see him jingle his keys, and has such utter contempt for reporters, analysts, and investors that he doesn’t have to prove AI is actually doing anything. Those writing up his earnings will do it for him.

Meta, on the other hand, has little real AI story, and can’t even seem to get its metrics straight on what AI is doing for the company, per my premium piece from earlier in the week:

This is an impressive-sounding stat that doesn’t actually connect to any meaningful revenue information, especially when Meta announced in January 2026 that doubling GEM’s compute allowed it to drive a 3.5% lift in ad clicks (a different measurement) on Facebook and “more than a 1% gain in conversions on Instagram” in Q4 2025, which is…4% lower.

Nevertheless, I have to give Microsoft and Amazon credit for deigning us worthy of actual numbers, even if they’re piss poor.

AI Revenues Are Pathetic and Circular, With OpenAI Representing 71%+ Of Microsoft’s AI Run Rate and Anthropic 80% of Amazon’s

In any case, I need you to recognize how small these numbers are in comparison to the capex it’s taken to make them.

To give you some context, Amazon’s AI revenue run rate is roughly 0.419% of the $298 billion in capex it spent on AI capex so far, or around 25% of the $5 billion it just invested in Anthropic last week. Microsoft, on the other hand, has spent $293.8 billion on AI capex through its latest quarter — making its revenue run rate around 1.04% of its spend.

These revenues are deeply embarrassing! I am not sure why this isn’t the common refrain! These fucknuts have spent over a trillion dollars on AI and all they have to show for it is either nothing, vague statements about “everything lifting because of AI,” or pathetic revenues that only get worse the more you think about them.

OpenAI Represents 70%+ Of Microsoft’s AI Revenue and 80%+ Of Its AI GPU Compute Capacity, Creating The Illusion Of Growth That’s Dependent On A Company That Will Lose $25 Billion+ In 2026

Yet things actually get worse when you think about the sources of that revenue, or perhaps I should say source, as both Microsoft and Amazon (and I’d argue Google too, but we don’t know its AI revenues) are heavily-dependent on their large, unsustainable sons — Anthropic and OpenAI.

I’ll explain. Microsoft claims that its $37 billion in AI revenue run rate has grown by 123% year-over-year, which means its run rate, not actual 2025 AI revenue, was about $16.59 billion in Q3 FY25, or around $1.38 billion a month or, if you assume that number is consistent over the quarter (it likely wasn’t), about $4.14 billion. Based on my own reporting from direct Azure revenue numbers, this would make OpenAI’s $2.947 billion in inference spend in that quarter around 71% ($11.7bn) of Microsoft’s Q3 FY2025 AI revenue run rate. That’s embarrassing!

Yet my reporting helps us be a little more annoying than that. Back in January 2025 — around Microsoft’s Q2FY2025 earnings — it announced that its AI revenue run rate had hit $13 billion, or around $1.083 billion a month (or $3.25bn a quarter or so). In that same quarter, OpenAI had spent $2.075 billion on inference on Azure, or 63.8% of Microsoft’s AI run rate.

This is particularly funny when you go back to the quarter before, where Microsoft CEO Satya Nadella low-balled that figure, claiming it would be $10 billion in annualized run rate, and specifically said the following:

"It's all inference," he said. "One of the things that may not be as evident is that we're not actually selling raw GPUs for other people to train."

The CEO added that the company is turning away requests to use their GPUs for training "because we have so much demand on inference."

That’s…not really what happened.

Today I can report, based on discussions with sources with direct knowledge of Azure revenue, that in Q2 FY2025, Microsoft brought in around $325.2 million in revenue via renting out GPUs and other AI infrastructure, and around $367 million in revenue from Microsoft 365 Copilot, or less than half of the $1.467 billion that OpenAI spent on inference.

If you’re curious, the next quarter (Q3FY2025), AI infrastructure brought in around $412 million, and Microsoft 365 brought around $300 million.

While my sourcing for Azure revenues cuts off at Q3 FY2025, my OpenAI inference and revenue share data goes out a further two quarters to Q4 FY2025 and Q1 FY2026 (so Q2 and Q3 of the calendar year 2025), as well as half of Q2FY2026, and we can make some fairly straightforward estimates as a result.

So, based on my reporting, OpenAI spent $3.648 billion dollars on inference in the third quarter of 2025 on Microsoft Azure, or around $14.4 billion on an annualized basis. While I only had half the fourth quarter’s numbers, I estimate that OpenAI’s annualized spend hit over $18.5 billion — or around $4.6 billion a quarter — by the end of the year, and that’s not accounting for things like Sora 2 or the launch of its Codex coding platform. In total, this puts its spend at an estimated $13 billion dollars on Azure just on inference, with billions more on training.

Sidenote: If you work at Microsoft Azure and want to talk to me about these numbers, my Signal is ezitron.76.

Yet Microsoft Azure isn’t the only place that Microsoft gets fed revenue from OpenAI.

All together, that puts OpenAI’s spend on Microsoft services at over $18 billion dollars in 2025, and it’s easy to see how that would grow to over $24 billion dollars on an annualized basis in the last quarter, or around $2 billion a month. Microsoft is OpenAI’s primary cloud provider, and I estimate that OpenAI represents around 70% of its AI revenue, while taking up the majority of its infrastructure. Otherwise, Microsoft’s 20 million Copilot 365 subscribers likely pay no more than $7 billion a year.

I also think that OpenAI is taking up the lion’s share of compute.

Considering that 67% of CoreWeave’s revenue came from Microsoft renting capacity for OpenAI, I also think that it’s fair to assume that 80% or more of Microsoft’s GPUs are taken up by OpenAI, though some might now be taken up by Anthropic, which agreed to spend $30 billion on Azure. I’ve also confirmed that Microsoft’s “Fairwater” data centers — which constitute (when finished) “hundreds of thousands of GPUs” — are entirely reserved for OpenAI.

Microsoft desperately wants you to think that this is a diverse, booming revenue stream, when in fact it’s spent around $293 billion in four years to make — when you remove OpenAI — less than $3 billion a quarter in revenue, not profit.

Booooooo! Booooooo!!!!!

Anthropic Accounts For 80%+ of Amazon’s AI Revenues And At Least 75% Of Its AI GPU Compute Capacity

As far as Amazon goes, things get a lot grimmer. As I mentioned earlier, in early April, per Reuters, Amazon’s Andy Jassy admitted that its “cloud business’ AI revenue run rate was more than $15 billion in the first quarter of 2026,” which translates to around $1.25 billion in monthly revenue, or roughly 0.419% of the $298.3 billion in capex it spent so far, or around 25% of the $5 billion it just invested in Anthropic two weeks ago.

I also think it’s reasonable to assume that a large part — if not the majority of — that revenue comes from Anthropic. Per my reporting last year, Anthropic spent $518.9 million on Amazon Web Services, at a time when it had around $7 billion in annualized revenue, a figure that’s increased by 500% (if you believe it) to $30 billion in annualized revenue since. $518.9 million is about $6.2 billion in annualized spend, and I think it’s fair to assume that its spend will have at least doubled to $12 billion in annualized revenue, or around 80% of Amazon’s AI revenue.

“Year-over-year” is an attempt to obfuscate actual growth in the era of AI. A better comparison would be quarter-over-quarter, which was 12% from Q4 2025 ($17.66 billion).

This is actually significant, because it’s a slower rate of growth than between Q3 and Q4 2025, when cloud revenue jumped from $15.15 billion to $17.66 billion, or 14.2% quarter-over-quarter).

I think quarter-over-quarter growth is far more indicative of how a business is going.

Google Cloud is far more than AI! It includes all of Google’s workspace revenue, such as Gmail, Google Docs, and so on. It’s important to remember that Google jacked up its workspace pricingtwice in 2025, and that by Q1 2026, the majority of customers will have been forced to renew at inflated prices. It also includes all of Google’s cloud revenue, which is incredibly diverse and far more than just AI compute.

Google has intentionally bucketed AI-related revenue into Google Cloud so that finance and tech journalists will claim that AI is what’s driving this growth despite there being no proof that that’s the case.

One of the reasons that Google might not want to break out its AI revenues is that they’re — much like Amazon — heavily-inflated by Anthropic’s compute spend. Sadly, we have only a little information about Anthropic’s spend outside of its promise to use “up to one million TPUs, with over a gigawatt of capacity [coming] online in 2026” from the end of last year, and a month ago, when it said it would use “multiple gigawatts of next-generation TPU capacity…starting in 2027.”

Another guess might be to travel back in time to before Anthropic was a huge consumer of compute. In Q4 2023, Google Cloud sat at about $9.19 billion a quarter, and $11.96 billion in Q4 2024 (around 23% year-over-year, but a putrid 5% quarter-over-quarter from Q3 2024). By Q2 2025, it sat at $13.62 billion, and as I mentioned above, accelerated to $15.15 billion to $17.66 billion (14.2% quarter-over-quarter) to $20 billion (11.7% quarter-over-quarter) in the following three quarters.

Explainer: So, to create an output, a Large Language Model does “inference,” and the more users a company has, the more it spends on cloud services to support their inference. As a result, Anthropic’s growth means that it’s spending way, way more on its core cloud providers — Amazon and Google — to provide its services.

The cloud segment posted a notable acceleration, driven by surging demand for GenAI solutions, resulting in the doubling of backlog and tripling of operating income with the inclusion of TPU hardware agreements as a new revenue stream.

Interesting. Interesting. Google appears to be planning to sell its TPUs — its own custom silicon it currently uses only for its own services and some of Anthropic’s — to a non-specific amount of unnamed customers, to the point that its remaining performance obligations jumped from $242.8 billion to $467.8 billion in the space of a quarter.

Aside: To be clear, RPOs refer to any revenue that Google might earn in the future, such as the tens of billions of dollars Anthropic has agreed to spend, every single annual or bi-annual workspace account, every single massive ads deal, and so on and so forth.

Nevertheless, that’s a remarkable jump, especially when you try and work out who they sell to- oh wait, we actually know!

Google also signed a multi-billion dollar deal to rent TPUs to Meta, per The Information, and is also discussing A) selling TPUs to Meta directly, and B) creating SPVs that will buy its own GPUs and lease them to others:

In addition to forging the Meta deal, Google has signed an agreement with an unidentified large investment firm to fund a joint venture that would lease TPUs to other customers, according to a person involved in that arrangement. Google is in talks with other investment firms to fund other such joint ventures.

To explain, Google is creating something called a special purpose vehicle — a company with one purpose — that it then funds along with an investment firm. The SPV then raises cash via debt, which it then uses to buy TPUs directly from Google.

Now, remember that Anthropic deal to use a million TPUs from last year? How about the deal with Broadcom (which makes TPUs for Google) and Google to use “multiple gigawatts” of TPUs starting in 2027?

It’s a pretty sweet deal for Google! Google pays Broadcom to develop TPUs, Anthropic pays Google to buy those TPUs once Broadcom builds them, Google installs those TPUs in a data center, and then Anthropic pays Google to rent them back.

This isn’t real demand!

Boo!!!!!! BOOOOOO!!!!!!

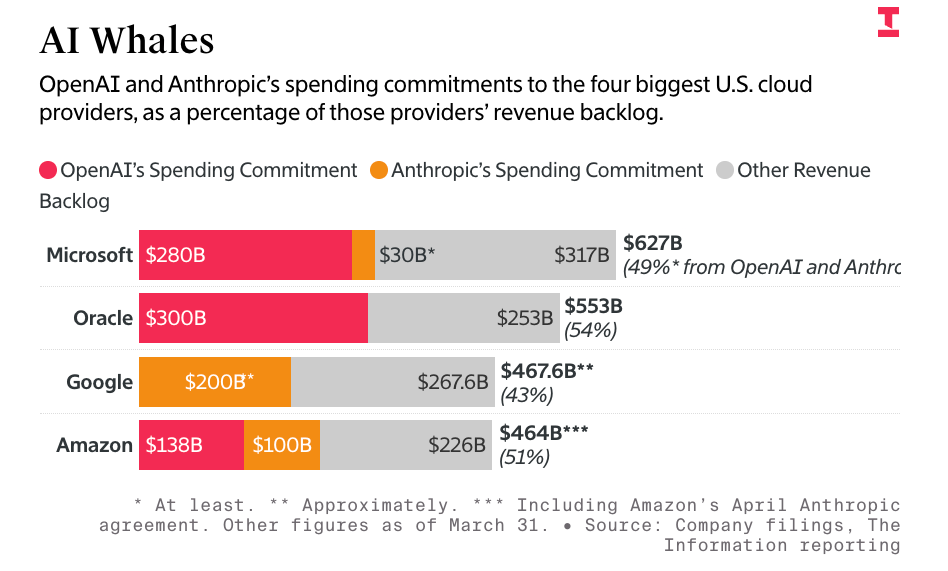

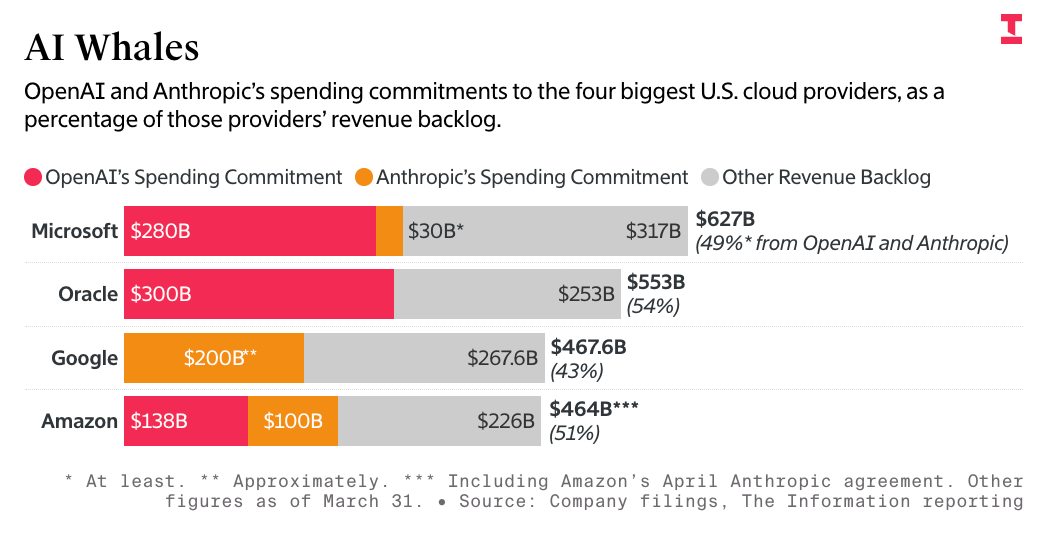

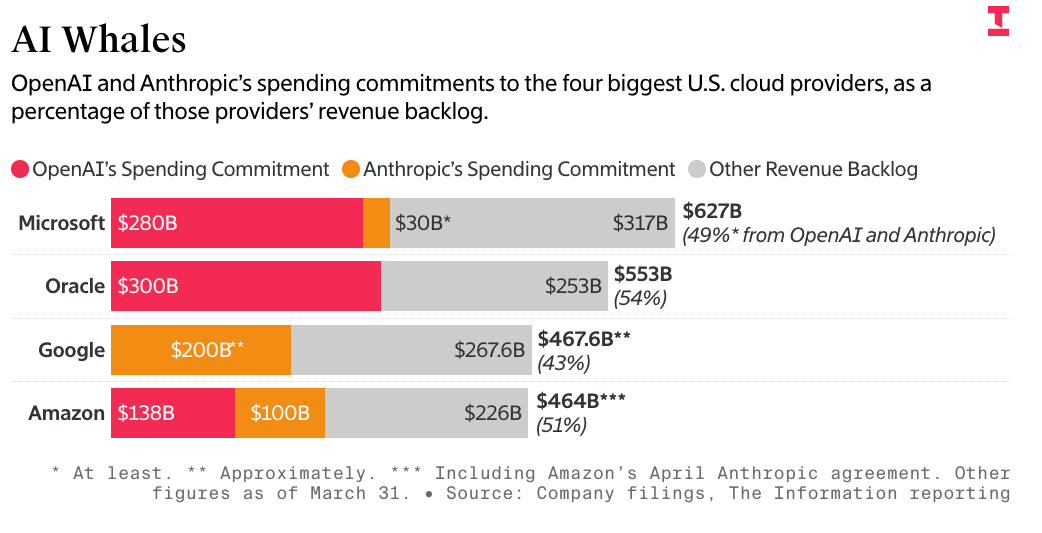

Anthropic Has Committed To Spend $200 Billion On Google Cloud and TPUs

So, for the sake of transparency, I wrote the above beforeThe Information published its story about how Anthropic had committed to spend $200 billion on Google Cloud and TPU chips, which contained this very important detail:

But as part of the deal, which begins next year, Anthropic plans to spend about $200 billion with Google over five years, according to a person with knowledge of it. The commitment means Anthropic represents more than 40% of the “revenue backlog” Google disclosed to investors last week, reflecting contractual commitments from its cloud customers.

Google, Microsoft and Amazon’s AI Revenues Are Almost Entirely Based on Circular Financing Relationships That Should Be Illegal

The Information’s story also had this fascinating chart showing that around 50% of Amazon, Google and Microsoft’s backlog (which includes all revenues not just AI) — a staggering amount — is made up of revenue from OpenAI and Anthropic:

To be clear, I also wrote the below before this chart ran, because it was very fucking obvious when you actually looked at the numbers.