Jan Kregel presented a great dinner speech at the recent Modern Monetary Theory Conference, touching on some of the fundamental ways we think about money and economics. (Sorry, no recording or transcript available.) I had a brief conversation with him afterwards, and we followed up with a few emails.

The quotation in the title of this post is condensed from the final line of one of his emails — a line that made me laugh out loud:

“So I guess we start from that — in the beginning was the word, and the word was the unit of account?”

Okay, yes: money-dweeb humor. But the implications are kind of profound.

The Word. Logos. Indeed. I’ve written about this before — how writing in its earliest forms emerged from tally sheets, accounting. Even, that its emergence was the first step on the road to outsourcing our memory onto iPhones, maybe even (only somewhat tongue in cheek) causing human brains to shrink over millennia.

Jan’s great line, and our conversations, prompt me to set down some thoughts on this ever-vexed subject. Herewith, twelve widespread usages and conceptions that, in my experience, tie our money discussions in knots. Please assume that anything you don’t like here is mine, not Jan’s, and apologies to those who have heard some of this from me before.

(A proleptic response to an inevitable digression: I’m assuming a closed national or world economy for simplicity. The “rest of world” sector, and the exchange rate with Martian currency, are not considered.)

#1. Money was invented around 700 BCE. No. That’s when coins were invented — handy physical tokens making it easy to transfer assets from one person’s (implicit) balance sheet to another’s. Money existed on something like balance sheets — tallies of who owns what and who owes what — long before that; those tallies go back thousands or tens of thousands of years. Mentions of monetary values in written documents — designated in staters, drachms, whatever — were widespread long before anyone thought of using coins for asset transfers.

The earliest coins, by the way, may well have been badges of honors and offices issued by religious authorities. Somehow people started exchanging them, and voila: physical currency. This had little or nothing to do with butchers and bakers or convenient time-shifting of purchases. That’s a made-up armchair myth (though the convenience benefit is real). Wampum, likewise, wasn’t used for trade exchange until Europeans captured that “money” system and transformed it.

#2. Money is a “medium of account.” (Whatever “medium” means in that phrase…) Money was invented when some clever tally-keeper, totting up cows and horses and bags of grain, invented the arbitrary unit of account — a unit that allows those heterogenous goods to be tallied on a single sheet, in a common unit of value. We find price lists of assorted goods on some of the earliest Sumerian tablets, for instance, and price lists can’t exist without a unit of account. It’s hard to know, but it seems like this clever technology might have been invented multiple times over the millennia.

If this historical tale holds water, the earliest forms of money were just…the value of tallied (balance-sheet) assets, with the value designated, denominated, in a unit of account. In the beginning…

By this thinking, an “asset” is a labeled balance-sheet entry, designating the value of an ownership claim — again, designated in a unit of account. These “asset” things only exist on balance sheets. The claims themselves may be informal — you own the apple on your kitchen counter by norm, convention, and common law. Or they may be formal, inscribed in one or more legal instruments and a supporting body of law and norms. The forms and terms of these ownership-claim instruments are myriad and diverse.

Money in this sense is the UofA-designated value of an ownership claim (perhaps formally recorded in an asset entry).

Ask a real-estate zillionaire, “how much money do you have”? The answer has nothing to do with physical dollars in wallets, or any particular class of ownership claims/assets that are tallied up in “monetary aggregates.” It’s about total assets or net worth — necessarily, designated in a unit of account.

The problem arises when we confute these two common meanings of the word. Start watching: you’ll often see it happen even within a single sentence. This ubiquitous muddle — trying to talk about two different things using the same word — has engendered unending confusion.

Both uses of the word are perfectly valid and useful; they just mean completely different things.

#3. There is such a thing as non-fiat money. Nope. (A better description is “consensus” money. The consensus is usually enforced by the fiat powers of a government, temple authorities, etc.) The consensus exchange or “face” value of precious-metal coins must always be higher than the market value of the metal substrate. If the reverse were true, people would just melt them down. Outside the fiat/consensus purview of the issuer, those coins many only retain their substrate value. So they’re still valuable for far-flung trade, or if authority breaks down, because the commodity may still retain consensus value. (That security in itself can contribute to holding up their consensus face value.)

Ditto cigarettes in POW camps. There are physical things called cigarettes, but there’s also this conceptual thing that emerges when people start using them in general trade: a “cigarette.” Or “the cigarette.” It’s a unit that can be used to designate the value of other things.

The consensus value of coins and currency is based on the stability of the unit of account. (See: Brazil.) The coins are just physical tokens representing a unit of exchange — an asset that can be transferred, and that’s designated in the unit of account. In the beginning…

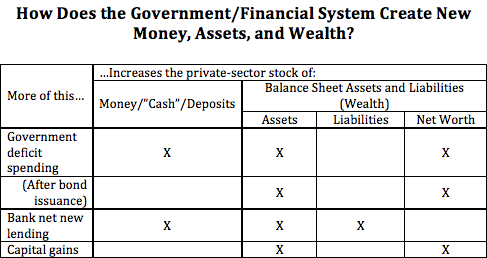

#4. Money “is” debt. Or, “you are paying with liabilities.” Money, by any definition, is always and everywhere an asset of the holder. The $5 bill in your pocket or the five dollars in your checking account are assets on your balance sheet. Paying, spending, is transferring assets to someone else — from the lefthand side of your balance sheet to the lefthand side of theirs.

Now of course money issuance is often associated with the creation of new balance-sheet liability entries — think government deficit spending — but those liabilities are posted to the money issuer’s balance sheet. The recipient gets an asset: the credit half of the tally stick. That’s what gets passed around in spending and payments. The debt side is generally held on the balance sheet of large, powerful creditors or institutional authorities.

This isn’t just true of “cash”; government bondholders are obviously holding assets. The debt is on the government balance sheet. “Holding debt” is a handy shorthand for finance types, but considered even briefly, it makes no literal sense at all. How could you hold or own something you owe?

Ditto “paying with liabilities.” If you transfer a liability from the righthand side of your balance sheet to the righthand side of another’s, you are unlikely to receive much thanks, or any value in return.

These usages can be useful, stylized ways of referring to particular economic, financial, and accounting relationships. Which is fine as long as users are perfectly clear on how the thinking is stylized. But on their face they don’t make sense, and they engender great confusion. Money is always an asset of the holder.

#5. People “spend out of income.” Spending, payments, always come from asset balances. That’s what payments are — asset transfers. When you write a check, you withdraw from your checking-account balance. When you buy a bag of Doritos at 7-11, the money’s coming out of your wallet. It’s impossible to “spend out of” the instantaneous event of somebody handing you a five-dollar bill. Once it’s in your hand, once it’s an asset you own, you can spend it.

“Spending out of income” is another of those common usages — a useful shorthand way to talk about spending more or less than you receive over a period. It’s an unconsidered commonplace that deeply confuses our conversations about money.

#6. There’s a difference between “inside” and “outside” money. After new money is issued, its origin is immaterial in the particular. Where did the $100 in your checking account “come from,” originally? Say I borrowed it, or got it in a tax refund, or whatever, then paid it to you. It’s impossible to say, and it doesn’t matter, where it came from.

New assets appear in account balances from 1. government deficit spending, 2. bank lending, and 3. holding gains. Then people swap them for other assets, or transfer them to pay for newly produced goods and services. Whether the money came from “inside” or “outside” sources (or holding gains), once it’s circulating among accounts, it’s just…money. As we all know, money is fungible.

Certainly, newly created liability entries associated with money issuance can be economically significant. And some particular financial instruments retain a meaningful and influential financial or economic (ultimately institutional) relationship to particular liability entries. But in the big picture once the money’s out there, it’s disconnected from its “inside” or “outside” origins.

#7. Monetary aggregates tell us how much “money” we have. The various monetary aggregates so beloved of monetarists (M0, M1, MZM…) share a common, unstated definition of “money”: financial instruments whose prices are institutionally pegged to the unit of account — physical coins and currency, checking account and money-market deposits, etc. Remember the 2008 headlines: “Money Market Fund ‘Breaks the Buck.’The institutional powers and practices of pegging are diverse, and institutional pegging can fail.

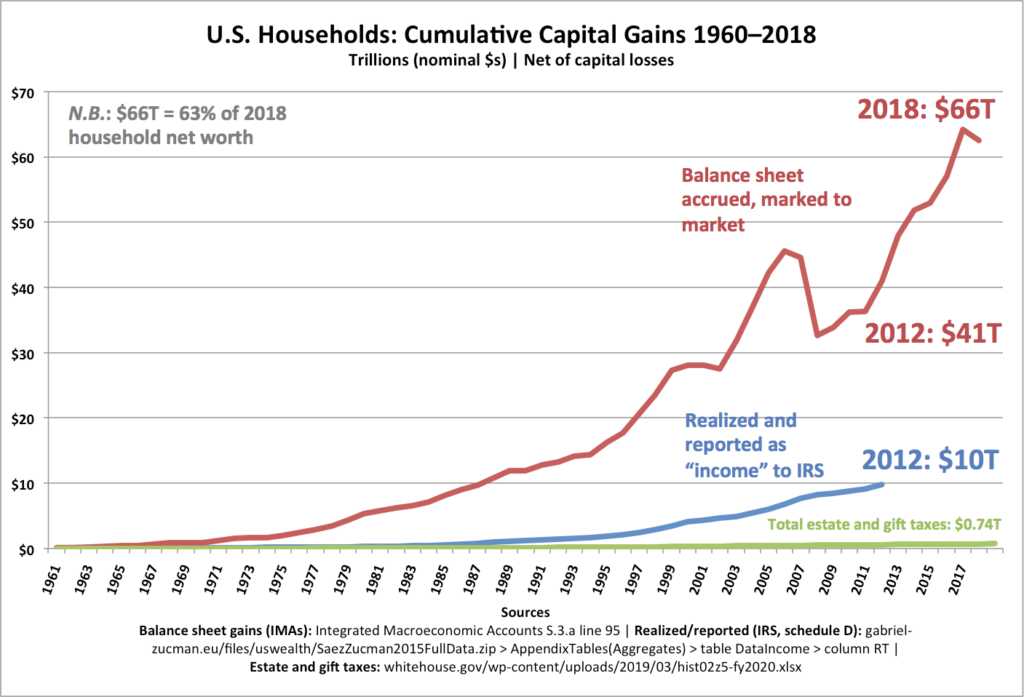

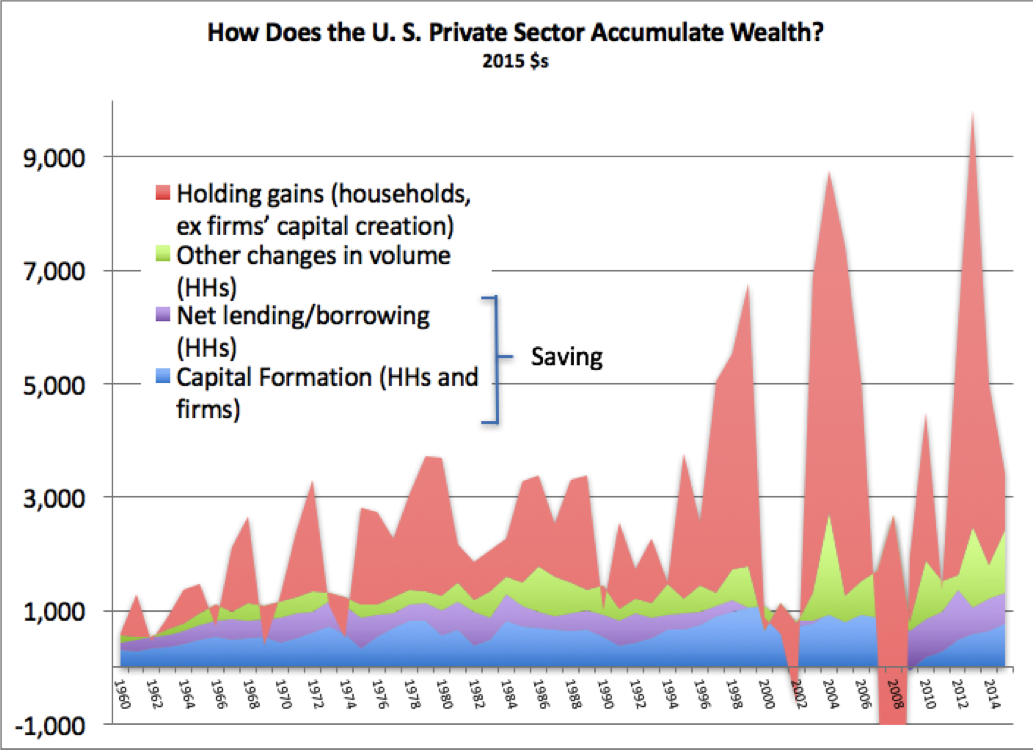

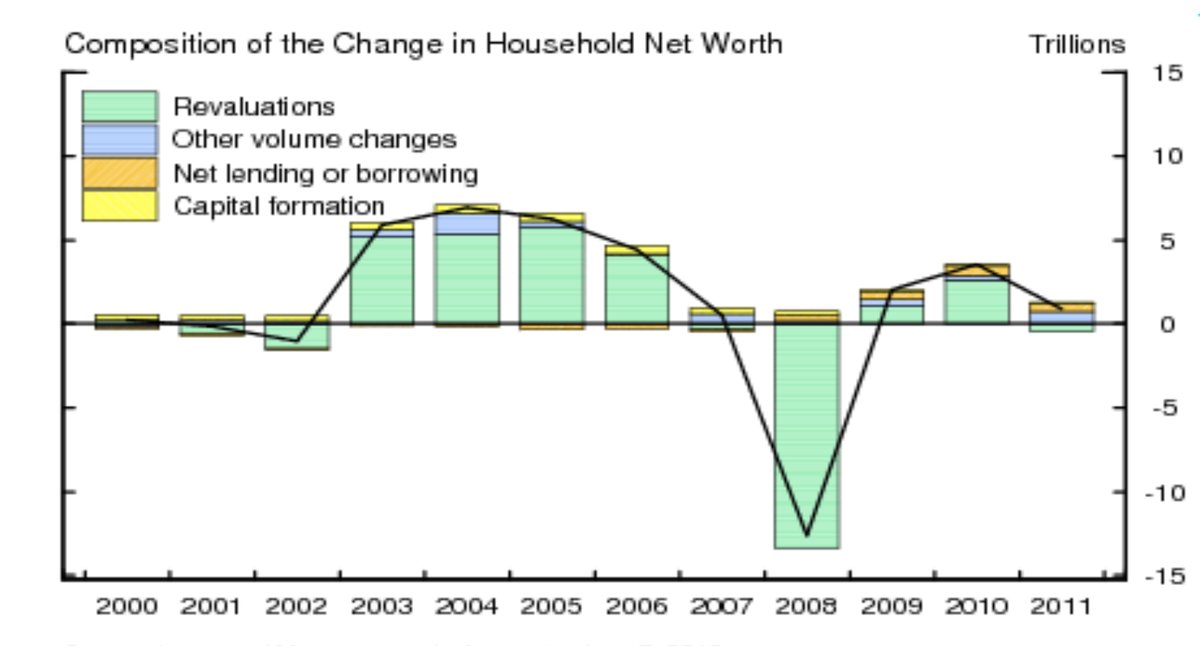

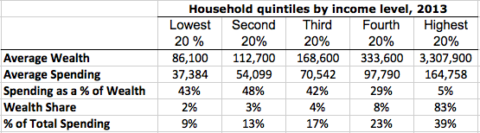

This particular subset of assets — fixed-price, UofA-pegged financial instruments — comprise only about 9% of U. S. households’ $111 trillion in assets. They play a particular role in individual and aggregate portfolio allocation (more below), they’re quite handy for buying new goods, and they’re a necessary intermediate holding for most asset swaps. But their stock quantity is swamped by even the price-driven change in other assets; capital gains on variable-priced instruments added $7 trillion to household balance sheets in 2013 alone. Monetarists’ fetishization of these “currency-like” financial instruments, and their aggregates, is…misplaced.

#8. If people save more money, there is more money (or “savings,” or “loanable funds”). Obviously, if you save (spend less than your income over a period), you have more money. But we don’t. Just, the money’s in your account. If you spent it instead of saving it, it would be in somebody else’s account.

Spending — even spending on consumption goods that you’ll devour within the period — is not consumption. The money isn’t, can’t be, “consumed” by spending. It’s created and destroyed by other, financial, mechanisms. If you eat less corn, we have more corn. If you spend less money, we have no more money.

#9. Saving “funds” investment. Investment spending, like all spending, comes from asset balances. “Funding” from flows is harder to nail down: If a firm this year has $1M in undistributed profits (saving) and borrows $1M, spends $1M on wages and buys $1M in drill presses, which inflow “funded” which outflow? Firms borrow to make payroll all the time. (Don’t even get me started on stock repurchases.)

I can’t resist quoting one of the best financial and economic thinkers out there (read the whole thread):

https://twitter.com/teasri/status/927908158877683712

Individual money-saving isn’t even really a flow; it’s a non-flow — not-spending — just an accounting residual of income minus expenditures. (Though of course it’s a flow measure: tallied over a period of time, not at a moment in time.)

#10. Portfolio allocations — and spending — are determined by “demand for money.” The relatively small stock of monetarists’ “money” — instruments whose prices are pegged to the unit of account — is sort of a fulcrum around which portfolio preferences and total asset value (wealth) adjusts. But the vague gesture toward the unmeasurable and dimensionless notion of “demand” is not illuminating. Here in more concrete terms:

Suppose government deficit-spends $1 trillion into private-sector checking accounts. The market’s portfolio is overweight cash (assuming portfolio allocation preferences are unchanged). But the market can’t get rid of those fixed-price instruments — certainly not by spending, which just transfers them — or change their aggregate value (their price is fixed, pegged to the unit of account).

So people buy variable-priced instruments — stocks, bonds, titles to real estate, etc. — bidding up their values competitively until the desired portfolio allocation is achieved. (This, by the way, is exactly how things work in the more advanced Godley/Lavoie-style, “stock-flow consistent” or SFC models.)

The economic implications of this: A trillion-dollar deficit-spend results in $1T more in private-sector assets (the “cash”), plus any asset-value runups from portfolio adjustments triggered by that cash infusion. (This is before even considering any effects on new-goods spending — the so-called “multiplier” — or the proportion of spending devoted to investment — Keynes’s particular fixation.)

Sure, if wealthholders are feeling nervous — more concerned with return of their wealth than returns on their wealth — they may prefer instruments that by their very nature guarantee stability, non-decline relative to the unit of account. They’ll sell variable-priced instruments, running down their prices until the market reaches its preferred portfolio allocation. “Liquidity preference” is one rather strained way to refer to this straightforward idea of portfolio allocation preferences.

Likewise, “demand for money” is a cute conceptual and verbal jiu-jitsu, flipping straightforward understandings of portfolio preferences on their heads. Demand is supposed to influence price and/or quantity. But it can’t influence the “price of money” or the aggregate stock of fixed-price instruments — only the prices, hence aggregate total, of variable-priced instruments. This notion does far more to confuse than to enlighten.

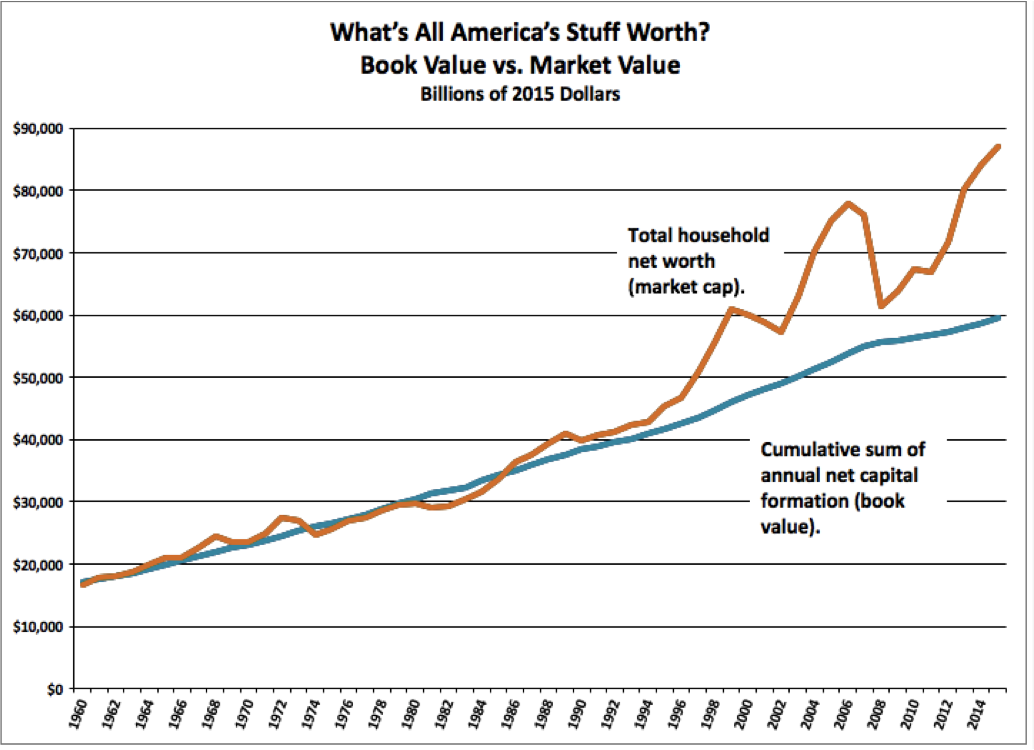

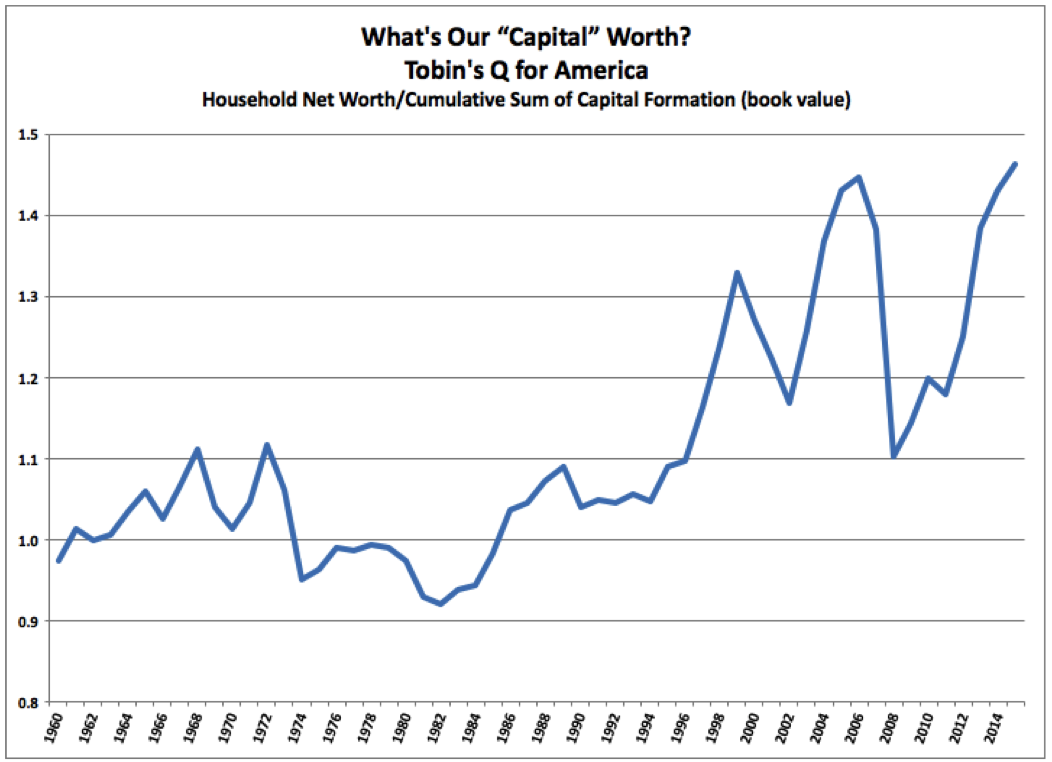

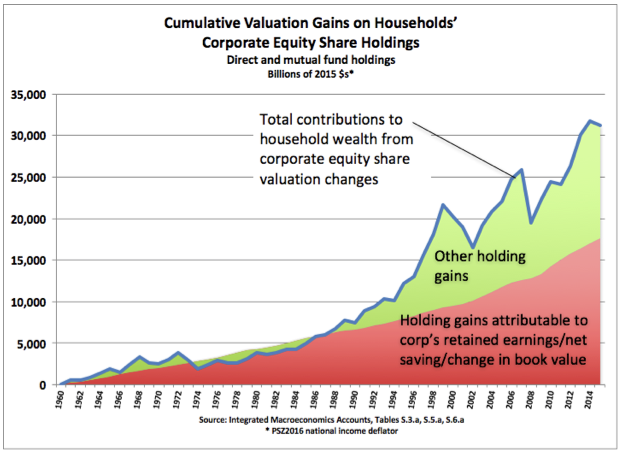

Takeaway: holding gains and losses — which are almost universally ignored in economic theory even though they’re the overwhelmingly dominant means of wealth accumulation — are the very mechanism of aggregate portfolio allocation. If you’re only considering “income”-related measures (which ignore cap gains), there’s no way to think coherently about how economies work.

#11. The interest rate is the “price of money.” This is like saying a car-rental fee is the price of a car. The price of a dollar (a unit of exchange) is always one, as designated in the dollar (the unit of account). The cost of borrowing is something else entirely. Like “demand for money,” “the price of money” is just verbal and conceptual gymnastics, inverting the very meaning of the word “price,” and trying to shoehorn money-thinking into a somewhat inchoate notion of supply and demand (that’s constantly refuted by evidence). It’s not helping.

#12. Central bank asset purchases are “money printing.” Not. Sure, the Fed magically “prints” a zillion dollars in reserves to purchase bonds. But then it just swaps those reserves for bonds, which are “retired” from the private sector onto the Fed’s balance sheet. Private-sector assets/net worth are unchanged; the private sector just has a different portfolio mix: more reserves, less bonds.

Ditto when the Fed sells the bonds back (as it’s now doing and promising to do, a bit); it re-absorbs the private sector’s reserve holdings and releases bonds in return, disappearing the reserves back into its magic hole in the ground. (As Milton Friedman observed, banks have both printing presses and furnaces.) Again: no accounting effect on private-sector assets or net worth.

QE and LSAPs do have some asset-price, hence balance-sheet, effect, at least while they’re happening; the central bank has to beat market prices by a smidge to play the whale and buy all those bonds. Bond prices go up and yields go down. Which will push investors’ portfolio allocations more into equities and other “risk assets,” driving up their prices some. But the first-order accounting effect is just to change private-sector portfolio allocations.

So there: twelve conceptions about money that have made it difficult or impossible for me, at least, to think coherently about the subject. Here’s hoping these thoughts are useful to others as well.

=============

I’d like to end this post with the same question for my gentle readers that I went to Jan with. Units of account are very odd conceptual constructs indeed. They’re not like other units of measurement — inches, degrees centigrade, etc. — which generally have some physical objective correlative: “length” or “warmth” or suchlike. Units of account tally “value,” which basically means value to humans, a function of human desire. And human desires, of course (“preferences”), vary.

So my question: what’s a good metaphorical or figurative comparison to help us understand and explain this strange conceptual thingamabob? Is money an invention like algebra? Are there other conceptual constructs that are similar to units of account, comparable mental entities that can help us think about what these things are? I can’t think of any good analogies. It’s vexing.

Extra points question: what is “the bitcoin”?

Yes: In the beginning was the word. Words are one of the main things, maybe the main thing, that we use to think together. All thanks to my gentle readers for any help in doing that.

Related posts:

- MMT and the Wealth of Nations, Revisited

- Actually, Only Banks Print Money

- The Giant Logical Hole in Monetarist Thinking: So-Called “Spending”

- Safe Assets, Collateral, and Portfolio Preferences

- No: Money Is Not Debt

{kind=link}