A historian’s perspective on how to deal with the Nobel frenzy I generally try to stay away from the Economics … More

Show full content

A historian’s perspective on how to deal with the Nobel frenzy

I generally try to stay away from the Economics Nobel frenzy, if only because the hyper-personalization of scientific achievements it entails it at odds with how we historians understand credit dynamics in science. Economics research has become increasingly collective, drawing on expertise in theory, data collection, empirical techniques, sometimes philosophy, law or psychology. There’s a tradeoff here, of course—one I’ve witnessed in the archives of the John Bates Clark Medal, awarded annually to an economist under 40 working in the US. These prizes generate expectations, divisions, and disappointments within the discipline, but they buy something valuable: prestige and visibility beyond it. They signal to the broader public that this work matters.

But I was one of the researchers asked to comment, almost live, on this year’s award on the French radio today, and as it happens, some good collective work by historians of economics on the 20th growth economics has been published recently. So here’s a post with a few references and thoughts. I won’t describe the laureates’ contributions because (1) the Nobel committee does that very well, (2) dozens of posts doing exactly that will appear in the next hours (see for instance Brian Albrecht at Econforces, the write-up of Mokyr’s work by Anton Howes, himself a great historian of technology, and watch out for Kevin Bryan’s always excellent summary on his blog A fine Theorem) and (3), the 2025 laureates happen to be excellent writers and vulgarizers, so just go read theirbooks.

Israeli-American economic historian Joël Mokyr received half of the prize, while French Philippe Aghion and Canadian Peter Howitt shared the other half. As has become common in the past decades, the prize is framed as a award for methods – not for results, not for policy recommendations, but primarily for methods.

Of course, the laureates do reach substantive conclusions. Mokyr demonstrates that sustained growth in the long run emerged from the combining two types of knowledge during the European renaissance: propositional knowledge (scientific knowledge on why things work) and prescriptive knowledge (practical knowledge on the how to make them work). This combination requires particular institutional and historical conditions, including political fragmentation, the Enlightenment, the development of a market of ideas in Europe whereby intellectual could challenge orthodoxy, and especially in Britain, a culture of progress. Building on Joseph Schumpeter, Aghion and Howitt argue that growth springs from creative destruction, a process whereby entrepreneurs try to escape competition by innovating to gain an edge over rivals.

But these conclusions haven’t gone unchallenged. Aghion and Howitt famously sparred with Stanford’s Charles Jones over the importance of R&D and population size and scale effects (as summarize by Acemoglu here and, see also this survey). Mokyr’s work provoked a controversy with Robert Allen over the causes of the British Industrial Revolution (see Crafts’s review of the controversy): was industrialization driven, as Mokyr argues, by cultural and scientific change—the circulation of ideas, Britain’s culture of progress and practical application? Or was it, as Allen contends, about higher wages, cheaper energy, and technical education? Behind these debates lies a deeper question: what fundamentally drives growth? Education (and which type)? Innovation? Learning by doing? Fertility? Geography? Institutions?

Economists disagree even more over these theories’ policy implications. What, then, constitute good competition policy? God industrial policy? Who should fund innovation and how? What level of intellectual property protection is appropriate? Can we pursue both decoupling and green growth simultaneously?

Ironically, shaping public policies is precisely why the Economics Nobel, or rather, the “Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel” was created. Avner Offer, Gabriel Soderberg and Phil Mirowski’s archival research reveal that the prize was a “coup” engineered in 1968 by Swedish central bank governor Per Åsbrink. After a decade of failed attempts to gain independence from Tage Erlander’s Social Democratic government—particularly the power to set interest rates autonomously—Åsbrink found another path. He would use central bank funds to establish an economics prize celebrating the institution’s tricentenary.

Advised by Assar Lindbeck, who would dominate the economics Nobel committee for the next 25 years, Åsbrink pressured the Nobel family patriarch into accepting the plan. The Nobel Foundation, then controlled by industrialists, approved. The announcement followed quickly. Like other science prizes, it would be administered by the Royal Swedish Academy of Sciences. “Economic science today is so developed and established as a scientific discipline,” Åsbrink declared, leaving no room for doubt. He believed rewarding this “science” would shift policy debates toward the monetary orthodoxy he favored.

The prize was, as Offer and Söderberg call it, a “vanity project”—explicitly designed to transfer sixty years of accumulated scientific prestige from physics, chemistry, and biology to economics. It succeeded spectacularly. Yet the authors find no systematic ideological pattern in the laureates who followed. The prize has simply become the public marker of what constitutes good economic science.

What these three economists got the 2025 Nobel for, then, is the new toolboxes they developed to study sustained growth. Mainstream economists may dispute their specific conclusions -how much innovation drives growth, what drives innovation itself- but they recognize that the methods have led to fruitful debates and contributions. And as usual, the Nobel committee has managed to walk a thin line between alternative approaches, bringing some together.

On one side: Aghion and Howitt’s mathematical model. They formalized Schumpeter’s creative destruction by building in microfoundations—showing how entrepreneurs’ choices generate and sustain innovation. It was a breakthrough compared to Solow’s seminal model (with exogeneous technical progress). Historians and writers have recently examined this shift, though with a greater focus on the work by Bob Lucas and Paul Romer, both earlier Nobel Prizes. Goulven Rubin, who has edited a recent special issue on the history of endogenous growth theory, outlines a puzzle at the heart of this story. Though several contributors have now won Nobels for their 1990s contributions, there was already a wave of endogenous growth models in the 1960s (think Arrow on learning-by-doing, Uzawa, Sheshinski, Shell and others). Why did the first wave falter while the second took off?

Perhaps because of these microfoundations. Perhaps also because their model was crafted in a way that allowed them to confront it with the new large firm-level datasets that were built in the decades. After the 1990s, Aghion has offered a range of empirical studies of the role of innovation in growth and the consequences of various types of policies, with a host of coauthors (see his recent work on how to subsidies car batteriesfor instance).

While the 1992 article for which Aghion and Howitt received the prize is representative of Aghion lifelong approach, for Howitt it represented just one step in a more eclectic intellectual journey. This comes through in another recent history of economics special issue, edited by Muriel Dal Pont and Hans-Michael Trautwein to celebrate Howitt receiving an honorary degree from Université Côte d’Azur. Tellingly, the special issue focuses neither on innovation nor on endogenous growth, but on the history of coordination failures in economics.

In their introduction, Dal Pont and Trautwein trace Howitt’s intellectual development, from the foundational influence of Keynes — see also the papers by David Laidler and Sylvie Rivot on how Howitt’s Keynesian commitments — through his contributions to disequilibrium theory à la Clower and Leijonhufvud, his joint work with Aghion, and most recently, his turn towards agent-based modeling to explain inflation. They see Howitt’s work as unifed by a single question “understand how market mechanisms can fail,” which requires addressing coordination issues in the short run (as macroeconomists usually do) and in the long-run. “In particular,” they write, “he sees adjustments to technological change not as a mere self-limiting transition to a new steady state but as a permanent condition of economic life in a progressing society, that is, a long-run phenomenon.” Howitt himself explains his approach in a contribution to the volume.

Even accounting for Aghion and Howitt’s diverging methodological paths, Mokyr is the outlier. He has few publications in top 5 journals. His methods are unambiguously historical. Now, rewarding economic historians is definitely a trend in the latest Nobel rounds (Acemoglu-Johnson-Robinson, Goldin, Bernanke), which is not quite reflected in the profession at large (for instance on the job market). But Mokyr’s approach stands as the most historical. He uses comparative analysis, waves together qualitative and quantitative evidence including correspondence, technical books, renaissance archives. He crafts narratives, he considers historical paths as unique.

Tanguy Le Fur’s work on the history of very long-run perspectives on growth among economic historians captures this tension. Having studied Oded Galor’s contributions, he’s now examining Mokyr’s. In the conclusion of his Galor paper, he notes that “the dichotomy between growth theory and economic history has thus been tackled by practitioners of both fields.” Yet here’s the irony: the Nobel committee has yoked together researchers working on the same question from different methodological perspectives, barely aware of each other’s work

How to approach the coming week of commentary, then? Expect rounds of applause and criticism, focused on different questions.

First, method. Are the laureates’ approaches appropriate? Nobel awards reflect methodological consensus within mainstream economics, so epistemological controversy will be muted—though whether Mokyr, or even Howitt, count as mainstream is debatable. Still, innovation and growth are central to heterodox traditions too, particularly evolutionary economics (see for instance the work by Richard Nelson, Sidney Winter and Giovanni Dosi, as well as Paul David’s economics of science approach to innovation. I mention these because they somehow rely on Schumpeterian framework, but there are so many others).

Second, conclusions: Does innovation drive sustained growth, or do other factors matter more?

Third, policy. If the laureates are right, what follows? What should industrial policy look like? Competition policy? Who funds innovation? For what? Given the prize’s history, media and publics will press laureates and commentators to weigh in on far broader policy questions—France’s Zucman tax, trade policy, Fed independence, debt levels, budget discipline. The Nobels’ authority will be invoked to legitimize political positions, often on topics the laureates never touched or framed differently.

Finally, the focus on growth and innovation itself including Aghion’s recent work with coauthors on innovation-driven energy transition—could itself become contentious. Some economists argue there’s too little attention to long-term drivers of European growth and innovation support. Others argue there’s too much focus on growth altogether—the green growth versus degrowth debate. (for some historical perspective on the dominance of the growth paradigm in economics, see Schmelzer’s history of growth theory, and his edited volume with Iris Borowy. There’s also a book by Christopher Jones just out this month, as well as this cool paper on mainstream vs ecological economists by Quentin Couix),

It is important that we, as researchers, medias and citizens, disentangle these different layers of conversations.

UncategorizedArrowBaumolBehavioral Economicscorporate social responsibilityCyert and MarchSurveystheory of the firm

Histories of Corporate Social Responsibility, part 2 In my first post, I examined existing research on the context, meaning and … More

Show full content

Histories of Corporate Social Responsibility, part 2

In my first post, I examined existing research on the context, meaning and legacy of Milton Friedman’s 1970 New York Times essay – the focal point of most histories of Corporate Social Responsibility (CSR) – and added my two cents based on archival data and my previous research on Friedman’s worldview. I made two points: (1) Friedman’s piece did not launch a “shareholder primacy” movement. By 1970, he was expressing what had become a minority view (more on this below). Nor did he “turn the tide.” The piece was influential, but citations and businessmen’s reactions were initially critical. It served as a trigger, but shifting corporate governance toward shareholder primacy required additional work (for instance Jensen-Meckling), a presidential election, shifts in business practices and a large wave of corporate takeovers – so this transformation only occurred at the turn of the 1990s. (2) Though Friedman’s mix of clarity and ambiguity has generated many interpretations, his goal was to write a political think piece aimed foremost at businessmen themselves. The focus on this single essay has therefore overshadowed the substantial literature that US economists produced on CSR between the 1950s and the 1970s – research that combined positive and normative analysis but usually stemmed from theoretical and empirical efforts to understand which objectives firms actually pursue.

This second post examines a sample of that research. While not exhaustive, I’ve selected studies that were (1) influential and (2) produced by economists who both worked on firm-related topics and wrote or testified specifically about CSR—criteria that significantly narrowed my sample (tell me who else I should cover in the comments!). I want to show how economists’ empirical work on firms shaped both their general views about whether companies should pursue goals beyond profit maximization andtheir opinions about whether such goals could be practically implemented. Summarizing their positions coherently has proven challenging—this remains very much work in progress and may evolve in coming weeks. Their normative stance on CSR emerged from their positive research, which was itself shaped by debates about what makes a good theoretical model of firm behavior and what counts as acceptable evidence.

Corporate Social Responsibility as an empirical fact, not just a normative goal

Before diving into the details of this work, let me establish the context. One crucial point is that when economists turned their attention to Corporate Social Responsibility after World War II, they did not do so because they supported its rise. Rather, they viewed this rise as an established fact worth studying. This is exemplifiedby Howard Bowen’s landmark 1953 book Social Responsibilities of Business. The Federal Council of Churches of Christ in America commissioned the book as part of a series on Christian ethics and economic life, and it included a full chapter on “Protestant views” of CSR. But it also examined changing social attitudes toward laissez-faire and featured two long chapters surveying businessmen’s own views of their social responsibility, based on hundreds of individual and collective statements by top executives from General Electric, Ford, and many other major companies, all listed in a detailed appendix. The book cited a 1946 Fortune poll showing that 93.5% of surveyed businessmen believed companies should consider social responsibilities, and 60% believed that at least half of US businessmen displayed such “social consciousness.”

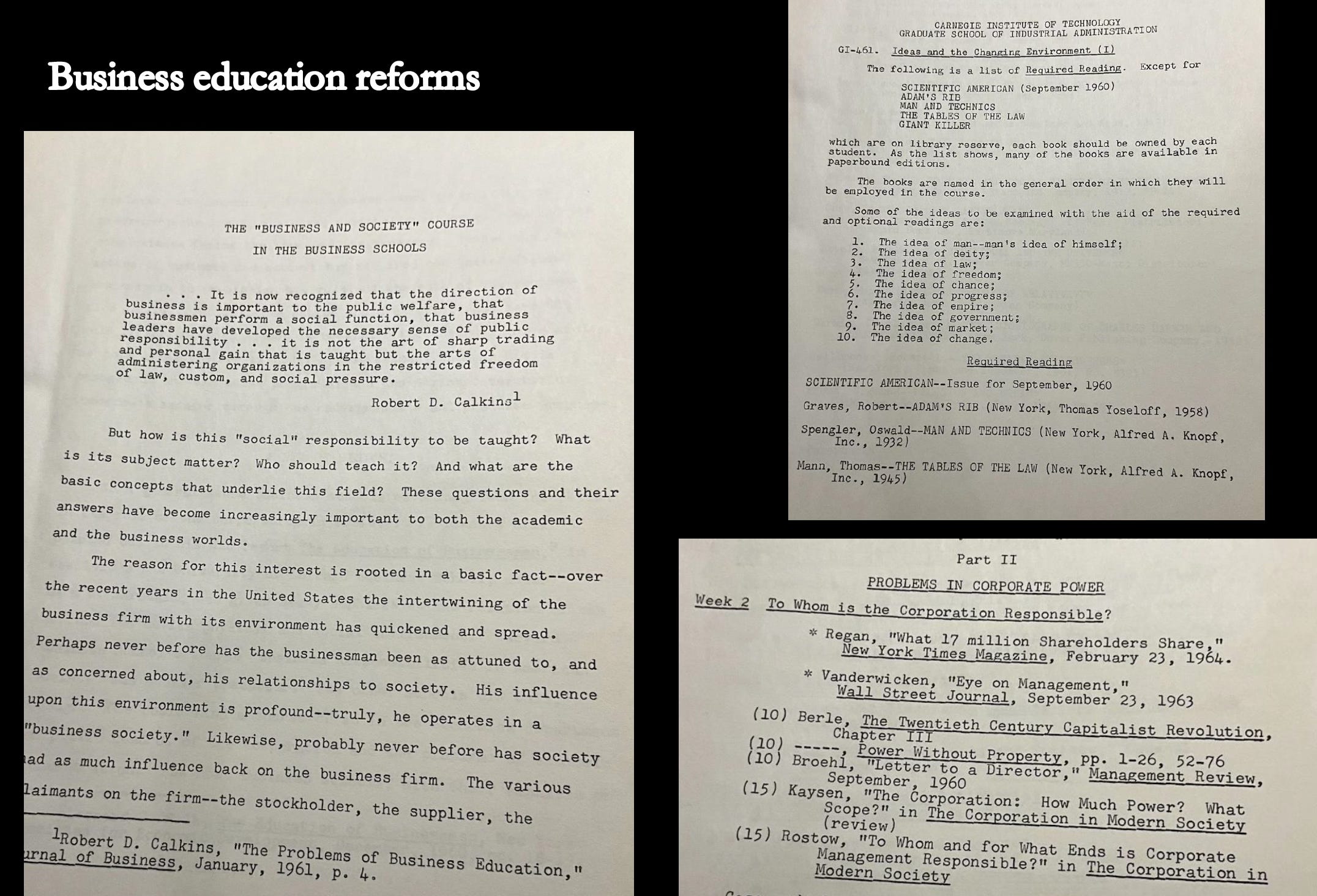

Businessmen’s soul-searching both fueled and was further encouraged by transformations in business education. In 1960, journalist Leonard Silk wrote a report on The Education of Businessmen for the Committee for Economic Development, following studies conducted by the Carnegie and Ford foundations. All advocated for “broadening the business school curriculum to include increased emphasis on the social role of business.” Business schools consequently established courses in business ethics on a massive scale. A 1960 report on “The ‘business and society’ course in the business school” opened with the question: “how is this ‘social responsibility’ to be taught?” Not whether, but how. While some professors assigned Thomas Mann, others gave students readings by Berle and a growing number of economists (including Kaysen and Rostow).

CEOs’ statements reflecting growing soul-searching as their companies had grown large enough to acquire market power that could shape the lives of workers, customers, and citizens were widely cited by researchers. Another source of evidence that sparked economic research was the related growth of corporate philanthropy and charitable donations. The year Bowen’s book was published, the New Jersey court issued A.P. Smith Manufacturing Co. v. Barlow, allowing corporate charitable donations for purposes other than direct business benefit. By the early 1970s, such donations had increased by 300%. Evidence of charitable giving by individuals was, as Philippe Fontaine has shown, a recurring entry point for theorizing social interactions (for scholars like Becker, Boulding or Vickrey) and empathy. Similarly, corporate charitable giving offered firm economists a pathway to writing about CSR. Indeed, most of Friedman’s archival folders on his 1970 piece contain data on corporate charitable giving, particularly to educational institutions, gathered by an independent researcher—he didn’t approve of the practice, much less the tax advantages the government offered.

Excerpt from Milton Friedman papers, Hoover, Stanford

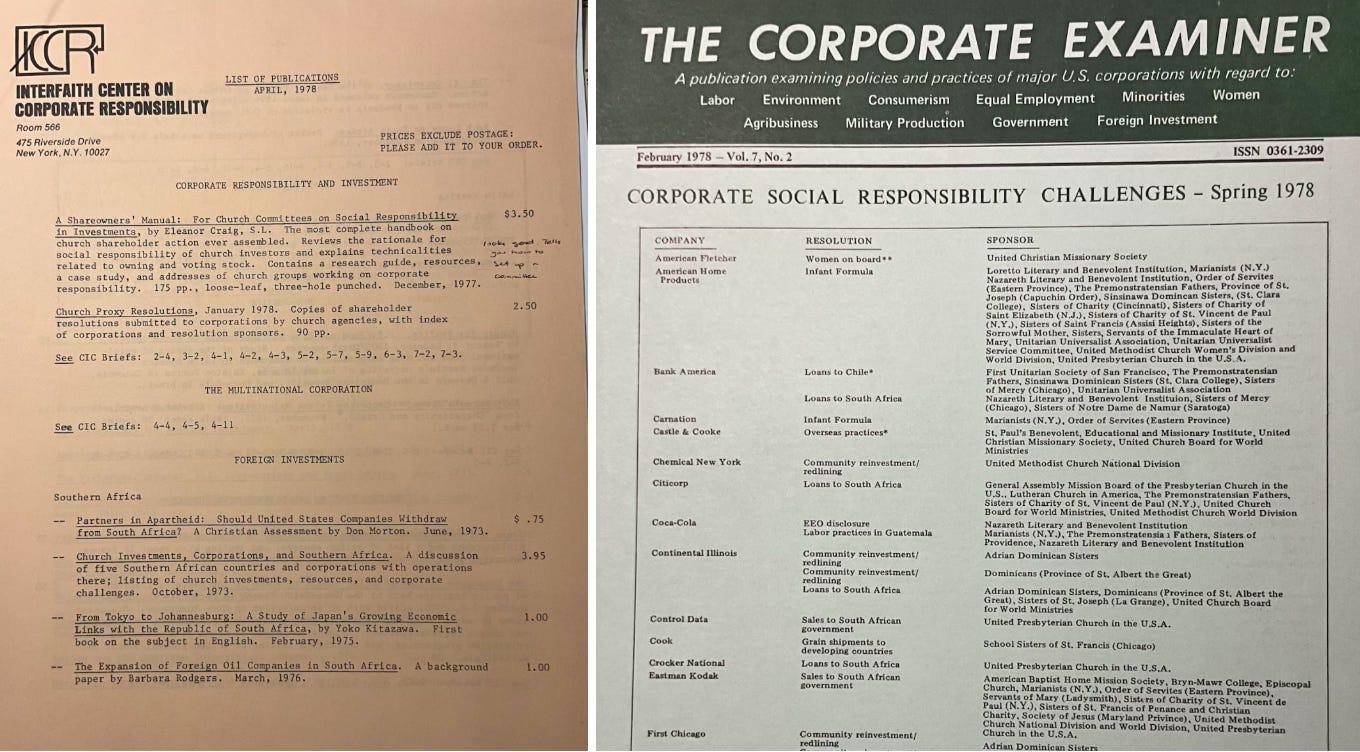

Beyond voluntary business initiatives, every segment of US society seemed to be calling for CSR, sometimes in reaction to growing evidence that business was causing harm. From the 1950s onward, the federal government passed a series of acts to protect workers and consumers on topics as broad as wages (1963), pollution (1969), and road safety (1966), and as specific as packaging (1960) and textiles (1958). Pollution and road safety, among other business scandals, were taken up by activists. They picketed against Dow’s production of napalm for the Vietnam War, wrote books on pesticides (Carson’s Silent Spring) and road safety (Nader’s Unsafe at Any Speed). Nader’s followers launched the GM campaign that formed the backdrop to Friedman’s 1970 Times piece, and techniques for pressuring corporations through divestment or shareholder activism were adopted by many groups. Below is an example from the archives of the Interfaith Center on Corporate Responsibility, which spent the 1970s and 1980s advising local churches on how to pressure major corporations into fighting sexism and diversifying boards of directors, refusing loans to South Africa due to apartheid, avoiding weapons or chemical sales, combating discrimination, and selling safer products like infant formula.

Excerpts from ICCR archives, Rubinstein Library, Duke University

Nader and other lobbyists convinced the government to consider federal chartering, and in 1976, Senate hearings were organized on “Corporate Rights and Responsibilities.” These included lawyers, activists, businessmen, and academics from management and economics.

It thus seemed that businesses pursuing objectives beyond profit maximization (taking into account the interests of what were increasingly called stakeholders) was both a collective aspiration and, despite the many business scandals of these decades, somehow an established fact. This was reflected in popular economic education. In the 1950s, the US Chamber of Commerce published a series of pamphlets designed to introduce citizens to basic questions that together formed “the American competitive enterprise system”: “The Mystery of Money,” “The National Income and Its Distribution,” “Demand, Supply and Prices,” along with pamphlets on taxes, labor, and “Why the Businessman?” This last one clearly stated that he was “assumed to have important social and community obligations.”

Economists on CSR : mixing positive research and social values

One academic path to the CSR debate was researching market failures. Kenneth Arrow perfectly exemplifies this approach. More or less in reaction to Friedman’s 1970 piece, he wrote a long column for non-economists in Public Policy. The title, “Social Responsibility and Economic Efficiency,” illustrates the mix of normative and positive arguments it contained, as did the paper’s opening question: “under what circumstances is it reasonable to expect a business firm to refrain from maximizing its profits because it will hurt others by doing so?” In it, he explained that “it is clearly desirable to have some idea of social responsibility, that is, to experience an obligation, whether ethical, moral, or legal,” but only because of the many market imperfections that prevent profits from reflecting the residual social good provided by firms. He quickly addressed congestion, returned several times to pollution and issues of chemical use, before turning to what he saw as a less understood problem: imperfect information. He then offered a popularization of Akerlof’s Market for Lemons (making no explicit reference to any specific research), describing at length how asymmetric information shaped and possibly destroyed used car markets.

Unlike Friedman, however, he didn’t merely discuss business’s voluntary focus on goals other than profit as a solution. He also mentioned regulation and taxes, discussed legal liabilities, before turning to voluntary CSR measures such as “codes of conduct” as guarantees for consumer safety. The latter “may seem to be a strange possibility for an economist to raise” but represents “a great contribution to economic efficiency,” Arrow explained, developing the example of medical ethics that he had encountered in his research on the medical sector. “Purely selfish behavior of individuals is really incompatible with any kind of settled economic life. There is almost invariably some element of trust and confidence,” he noted. But in the end, he didn’t believe these “desirable” codes of conduct could be implemented in areas other than medicine because of the lack of enforcement mechanisms, even social ones (“pressures”). If society wanted a solution to pollution, ethical codes were wishful thinking, regulation wasn’t flexible enough, and litigation wouldn’t work for “continuing problems.” The best option was taxes. Arrow’s research therefore informed both his view of CSR’s desirability and his assessment of its practical impossibility.

The same ambiguities pervade William Baumol’s approach to CSR, which combined theoretical models of how firms behave, confidence in businessmen’s morality, and doubts about implementing corporate objectives beyond profit. Here too, disentangling positive from normative elements of his intellectual development is difficult. As Alexandre Chirat has documented here and here [French], Baumol developed his theory of firm behavior through constant exchange with other economists who came to be grouped together as the “managerialists.” These economists had very different epistemological preferences, but together they produced work that challenged the idea that firms maximize profit. They all endorsed Berle and Means’s diagnosis that large corporations were now characterized by a separation of control and ownership, and they sought to understand the social consequences of the discretionary power recently acquired by managers, or as Galbraith wrote, the “technostructure.” In 1958-1959, exchanges with Galbraith pushed Baumol—the Princeton all-around theorist equally interested in welfare economics, growth, money demand, macroeconomics, and entrepreneurship—to develop and model the view that in oligopolistic markets, managers don’t maximize profit but rather sales.

Baumol relied on standard mathematical marginalist models, an approach that Harvard professor, diplomat, and Kennedy advisor Galbraith rejected in his books investigating the evolution of capitalist structures (American Capitalism, 1952) and consumers (The Affluent Society, 1958). As he worked on the next volume of his trilogy, The New Industrial State (1967), he articulated more clearly what he thought were the goals of the “technostructure” and, given its rising power, its influence on society at large: first, survival, and “once it is ensured by a minimum level of earnings…the greatest possible rate of corporate growth as measured in sales” (not revenue as for Baumol). Oligopolistic firms were influential enough to affect the functional distribution of income and even business cycles. Another member of that group was Cambridge institutional theorist Robin Marris, who instead considered that what firms maximize is the growth of corporate capital.

Though he wasn’t an economist, the group also came to include Berle who, after collaborating with institutional economist Gardiner Means, had famously debated CSR with law professor Frank Dodd in the Harvard Business Review. Berle feared that now unchecked managers would form a “tiny, self-perpetuating oligarchy” and should discipline themselves by pursuing stockholders’ interests—that is, profit. Dodd countered that “public opinion, which ultimately makes law [viewed] the business corporation as an economic institution which has a social service as well as a profit making function.” In a 1954 book, Berle conceded. He argued that Dodd was right and that “[t]he corporation, almost against its will, has been compelled to assume in appreciable part the role of conscience-carrier of twentieth-century… society.”

As Harvard industrial organization specialist Ed Mason pointed out, this trust in managers’ social conscience was shared by Baumol, Galbraith, and other managerial theorists. Calling them “corporate apologists,” he saw in all of them a belief that businessmen indeed exhibited a social conscience—a willingness to participate in the public good, whether because of their training, protestant ethics, or the social ethos of the day. Monopolistic power thus didn’t have the deleterious effects one might have expected.

By the turn of the 1970s, Baumol held positive views that firms’ objective was not profit, plus an additional belief that managers were somewhat guided by social conscience. As he turned more specifically to CSR, you would thus expect him to endorse it. But just like Arrow, his writings display skepticism that leaving the resolution of social problems to voluntary measures by business would work. Baumol contributed one of three 1970 articles that formed the research material for a Committee on Economic Development report on “Social Responsibilities of Business Corporations.” The main argument was that taking stakeholders’ interests into account was not inconsistent with shareholders’ long-term goals. The CED report called this complementarity “the doctrine of enlightened self-interest.” The term came from Baumol’s title (“Enlightened Self-Interest and Corporate Philanthropy”). He sought to explain why corporations had come to supply 5% of total private philanthropy in the US. He provided extensive data and concluded that this level of giving could not merely be explained by enlightened self-interest defined as concern for public image and social conscience. So he added another “self-enlightened” motive: the provision of public goods. Because they were non-excludable, they were in short supply, yet crucial to corporations’ long-term profitability. Indeed, 40% of corporate gifts went to education, then hospitals. “As businessmen see more clearly and are able to show more effectively to their stockholders that the company’s prosperity depends on the health of the communities in which it operates, it will become clearer that self-interest is indeed served by corporate contributions,” he concluded.

A few years later, Baumol returned to CSR with less optimistic conclusions. From the outset, he explained that “the primary job of business is to make money for its stockholders,” and that a “massive outburst of altruism” is neither desirable (it would be tokenism, and “business is likely to prove inefficient as a voluntary healer of the ills of society”) nor achievable. He didn’t seem to believe that social goals and profit maximization were generally consistent with one another in the long term. At that time, Baumol and William Oates had proposed cost-efficient set-ups for pollution taxes because Pigovian taxes seemed impossible to implement. The pair was working on their book The Theory of Environmental Policy. Addressing pollution as well as consumer safety problems was thus paramount in his piece. He focused on the failure of voluntary social responsibility initiatives by corporations. He repeated that he didn’t see businessmen as having less “integrity” than the rest of the population, but reminded readers that voluntary anti-pollution initiatives would probably result in loss of competitive advantage. So the only solution was changes in the corporate environment’s rules (such as taxes that would make polluting “costly”).

Baumol’s paper was reprinted in a 1975 volume on Altruism, Morality and Economic Theory edited by Edmund Phelps. This shows the broader intellectual context shaping economists’ CSR research at that time, but also how attempts to integrate altruism into theories of firm behavior diverged from economists’ modeling efforts to integrate other-regarding preferences in models of individual behavior. Phelps’s project explicitly aimed to move from this early research to a comprehensive “theory of altruism” as a solution to opportunistic behavior when information is imperfect—the same concern that motivated Arrow’s work. But like Arrow’s analysis, the corporate altruism chapters in Phelps’s book delivered disappointing conclusions. Alongside Baumol’s skeptical assessment, former RAND researcher Roland McKean contributed an equally pessimistic analysis of corporate “non-rule oriented unselfishness” across defense, environmental, and apartheid contexts. McKean’s verdict was blunt: “If we wish to alter business behavior affecting health or environment, we must turn to legislation and formal means of enforcement,”he concluded, citing Dales’s work on pollution rights and transaction costs more generally.

The same blend of positive research, moral endorsement, and practical skepticism emerged among a third group of economists who were also challenging profit maximization as the sole driver of firm behavior. At Carnegie, Herbert Simon had developed his bounded rationality approach specifically to explain actual business decision-making within firms—work that his colleagues Richard Cyert and James March would extend in significant ways.

Their 1963 collaboration, A Behavioral Theory of the Firm, proposed a positive theory of how organizations actually form collective goals. Their theory held that firm goals derive from a dual process of bargaining and learning, whereby individuals with conflicting interests and bounded rationality come to form an organization. “As a result,” they wrote, “recent theories of organizational objectives describe goals as the result of a continuous bargaining-learning process. Such a process will not necessarily produce consistent goals.” Their goal was to challenge “neoclassical” theories of the firm where, as Cyert and Charles Hendriks remarked, “even the sole objective of the firm, profit maximization, is determined by the environment because any other behavior of the firm will lead to its extinction.” A graduate student working on their book—which featured contributions by team members beyond the core text by Cyert and March—was Oliver Williamson. His transaction cost theory was influenced by this Carnegie context and sought to bridge the (economics) theory of the firm and the (management) theory of organization, as well as rational and behavioral models of individual decision-making.

While Cyert and March applied their behavioral framework to organizational choices as well as production, pricing, and investment behavior, the aforementioned 1976 Senate hearings offered an opportunity for Cyert to address CSR concerns. By then Carnegie’s president, Cyert offered a testimony in which he acknowledged that a series of corporate scandals, together with firms’ increased size, legitimately raised social responsibility concerns. But citing his work and Williamson’s on organizational structure, he explained that vertical integration was indeed a response to the uncertain environment in which corporations operated—one that allowed them to gather and process information. Antitrust policies “which are directed toward enforcing competition by enforcing uncertainty, by restricting the exchange of information,” should therefore be rejected. He concluded that “to retain the discipline of competition that pushes for lower prices, higher quality—the consumerism aspect of competition—we must rely increasingly on the ability of businessmen to behave like statesmen.” Cyert’s positive theory of the firm had thus led him to endorse a “trust businessmen” approach.

Why Economists Disagreed on CSR: Diverging Approaches to Theory and Empirical Methods

My interpretation of economists’ debates on CSR from these decades goes beyond noting their reliance on a mix of positive and normative arguments that are sometimes difficult to disentangle. Underlying their disagreement on whether corporations do and should pursue goals other than profit were diverging approaches to both theoretical modeling and what constitutes acceptable empirical evidence – what historians and philosophers often call “epistemic values.” That’s an interesting takeaway given that economists have shownrenewed interest in CSR after decades of neglect (next post), raising the question of how their new models and empirical designs shape this latest round of research.

Epistemic debates, for instance, pervaded the 1940s exchanges over firm maximization behavior, known as the “marginalist controversy.” What began as a debate about the consequences of raising the minimum wage evolved into a broader dispute over the relevance of marginalist theory—specifically, how firms actually set prices and wages. Labor economist Richard Lester challenged the idea that business decisions had anything to do with profit maximization and related calculations, while Austrian economist Fritz Machlup and Chicago theorist George Stigler argued that Lester had fundamentally misunderstood how formal theory should be applied. This was the debate that Friedman addressed in his influential 1953 methodological essay, which endorsed the inescapable lack of realism in modeling hypotheses as necessary for developing parsimonious yet widely applicable theories of human behavior.

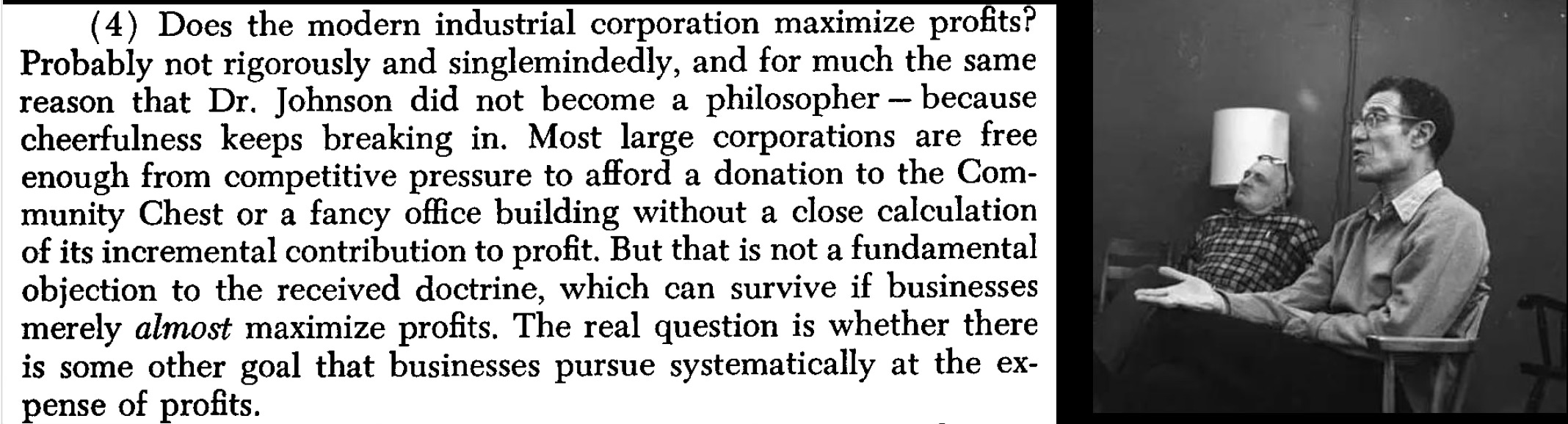

The status of (unrealistic) theoretical assumptions surfaced again in the 1960s-1970s debates around CSR. Galbraith’s The New Industrial State wasn’t simply arguing that firms don’t maximize profit – it mounted an epistemological attack against those economic theorists who dared employing conventional mathematical equations reflecting profit-maximizing firms, rational consumers, and efficient markets. Such modeling, he contended, represented either gross misunderstanding or deliberate misrepresentation of economic reality. Bob Solow responded with a scathing review in The Public Interest, defending profit maximization as a legitimate theoretical hypothesis among other counterarguments:

Galbraith doubled down in a rejoinder and suggested that such assumptions not only reflected bad methods but also ideological biases (Verena Halsmayer and Eric Hounshell thoroughly analyze the controversy here).

All these controversies were equally empirical—that is, economists’ stance on CSR largely relied on which empirical evidence they saw as acceptable (remember Bowen’s long list of CEOs’ statements). One method that proved central and contentious in research on firm behavior was the use of surveys. It was pivotal in the 1940s marginalist controversy, as Lester’s attack on the idea that prices and wages are set to maximize profit relied on questionnaires sent to 430 businessmen asking how they would respond to wage increases—they responded that they would not lay off workers but rather try to improve efficiency and increase their sales efforts. Both Machlup and Stigler criticized the method. Questions were badly phrased and proved nothing, the first argued. “We shall not accept this result even if Lester obtains it from 6,000 metal-working firms,” Stigler declared.

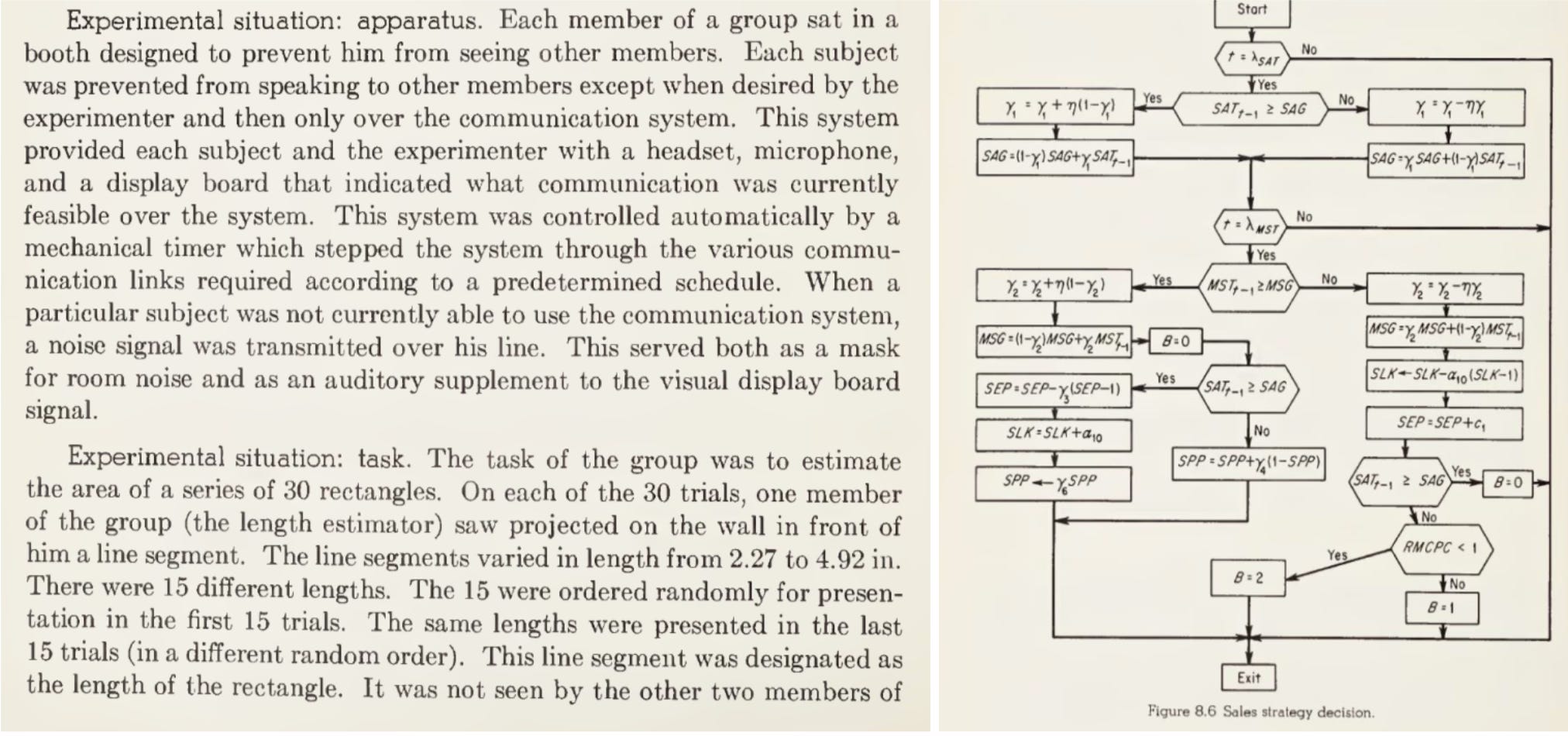

From the start, the Carnegie behavioral program had aimed to unite theoretical research with rigorous and novel empirical techniques. At the AEA in December 1961, Simon’s lecture about new developments in the theory of the firmencapsulated its ambiguous views of surveys. He argued that “management scientists are not concerned with systematic surveys of business practices” because it was impossible to generalize from them and because self-reporting was “lacking independent checks of actual behavior.” At the same time, he cautioned against dismissing this type of evidence. He pointed to intensive interviews and on-site observation studies (costly and also difficult to scale up), as well as laboratory experiments and computer simulation as rising empirical techniques to test alternative theories of firm behavior. The Cyert-March book relied on a combination of such techniques: a long appendix presented simulations of a complex decision model developed by Cyert and K.J. Cohen and inspired by Forrester and Orcutt’s work. One of the chapters introduced experiments by Cyert, March, and William Dill: they tested their administration graduate students to understand how framing and communicating investment choices affect decisions, and had their undergraduates play a team game in the lab to understand information processing and conflict resolution under various sets of rules. Recent empirical research on CSR largely relies on such games and surveys embedded in physical or online lab settings: how much is the acceptance of their results underpinned by the changing status of these methods?

Excerpt from Cyert and March (1963)

Overall, these economists mixed theoretical and empirical, positive and normative arguments to develop complex stances on CSR: they rejected profit maximization as an accurate depiction of business behavior, generally believed that businessmen possessed social consciences and should care about their impact on stakeholders and social problems, yet often doubted that voluntary initiatives running counter to stockholders’ short-term interests could be reliably sustained. This complexity illustrates a point Columbia law professor Dorothy Lund made at a recent conference when we discussed why the “shareholder view” of corporate governance seems stickierthan the “stakeholder” alternative. She attributed this to the lack of consistent legal foundations for the stakeholder view, and my account suggests that in economics too, the rationale for CSR was often more plural and diffuse than arguments against it.

The likes of Friedman and Henry Manne, who outright rejected any appeal to CSR, were actually a minority at the time. Throughout the 1970s, CSR opponents built on theorists like Armen Alchian and Harold Demsetz to develop a theory of the firm as a nexus of contracts. The making of Jensen and Meckling’s work—the topic of my final post—connects to a question I can’t definitively answer. While their contribution is usually credited with providing intellectual foundations for both law and economics and the “shareholder primacy” approach in business, I wonder whether it instead killed mainstream economists’ interest in CSR for the next three decades.

This post belongs to a series exploring how economists have historically approached Corporate Social Responsibility (CSR). This is research very much in progress, aimed at fostering conversations with CSR researchers across economics, management, and law, while helping me develop lectures on the intersection of economic history and business. I’ve been teaching about economists who shaped—and were shaped by—20th-century public policy. But I’ve grown increasingly frustrated at my inability to offer a parallel lecture on the private sector. There’s much less work on how economists have conceived the firm theoretically, studied business practices empirically, and shaped them through advising. This gap exists mainly because we have far fewer sources available compared to public policy research.

Researching economists’ historical approach to CSR essentially means examining how they’ve answered a fundamental question: What is or should be the corporation’s primary goal? In whose interests should corporations operate? To whom are they legally accountable? Or, in economic terms, what’s the firm’s objective function? These multiple, overlapping formulations reveal the ambiguities that run throughout this story: twin questions—some positive (about what is), others normative (about should be). Twin vocabularies: some straightforwardly “economish,” the type found in industrial organization papers in academic journals; others drawing from the language used by economists in business schools, management scholars, and practicing managers; and still others employed by corporate law scholars interested in what the “corporation” fundamentally represents—whether it serves shareholders, managers, stakeholders; whether it exists as an independent legal entity.

Histories of CSR in the 20th centuryabound, but these are mostly written by historians of management and corporate law scholars. When these accounts feature economists, they either focus on an era before economics and management had separated as disciplines (like the 1930s Berle-Means versus Dodd debate) or on later economists housed in business schools that, as Rakesh Khurana and Marion Fourcade observed, had restructured themselves along the lines of economics departments, once again blurring disciplinary boundaries (think Carroll, Jones, Freeman, Porter). The rise of finance as an intermediary field adds further complexity. These historical narratives nevertheless reflect their authors’ disciplinary backgrounds. Most management scholars present an inexorable, continuous rise of CSR scholarship, chronicling the successive emergence of stakeholder theory, sustainable development, strategic CSR, shared value, and ESG investing. Finance specialists, by contrast, emphasize the ascendancy of shareholder primacy. My goal is to understand what a distinctly economics-oriented narrative might look like.

A few longer historical perspectives have emerged in recent years. The volume edited by David Chan Smith and William Pettigrew traces business-society relationships back to America’s emerging non-profit sector, the Muscovy Company of 1555 (England’s first joint-stock company), medieval uses of the term “corporate,” and even the Code of Hammurabi. David Gindis’s special issue examines the English East India Company and its merchant guild predecessor the Levant Company in the 1600s, traces limited liability concepts from the 17th century, and analyzes Ernst Freund’s work on corporations’ legal nature.”

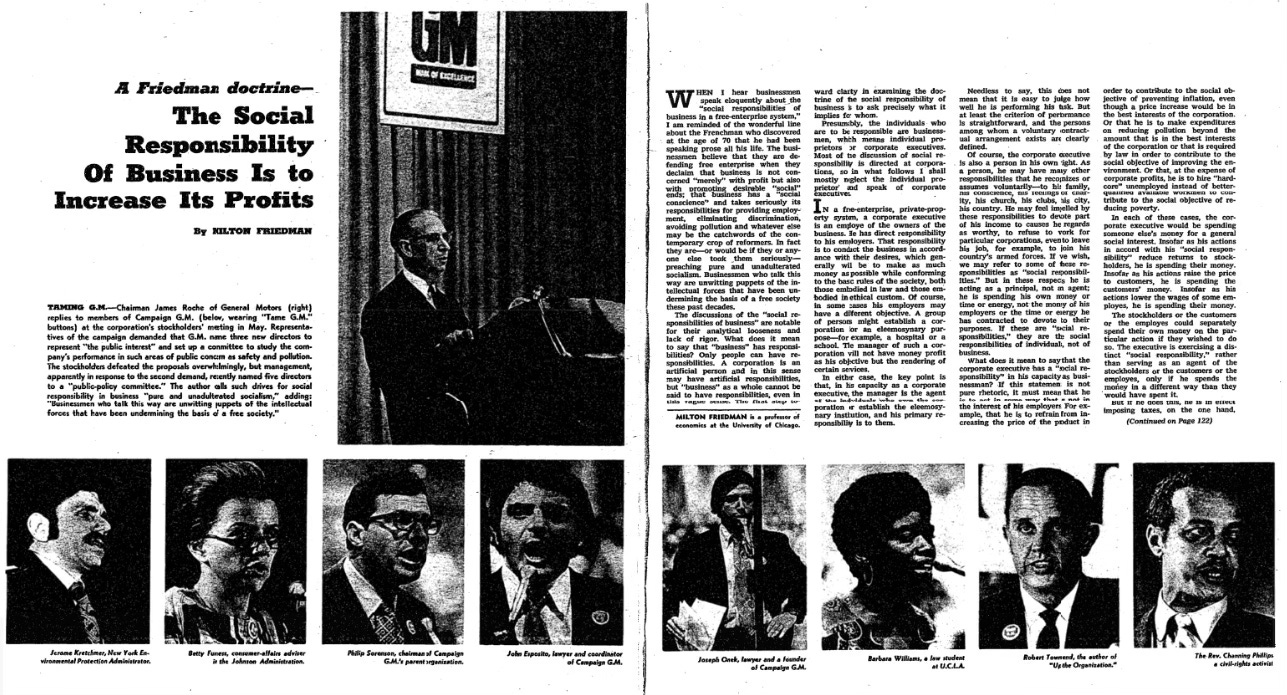

Whatever their disciplinary, geographical, or historical scope, all existing histories of corporate social responsibility share one thing in common: Milton Friedman’s 1970 New York Times piece, “The Social Responsibility of Business Is to Increase Its Profits.” Super-titled “A Friedman Doctrine” likely by the Times editors, this article has been widely credited with reshaping a century-long debate over corporate purpose and spearheading the shareholder primacy movement. Wrongly so, as corporate law professor Brian Cheffins recently demonstrated—and I agree with his assessment (more on this below). See his piece “Stop Blaming Milton Friedman!” for a thorough review of how Friedman’s article became canonized. The piece now appears to be Friedman’s most cited work, with over 30,000 citations according to Google Scholar—slightly surpassing Capitalism and Freedom and cited three times more than the academic works that actually earned him fame: A Monetary History of the United States and his Nobel Prize-winning Theory of the Consumption Function.

The irony is striking! Friedman devoted exactly four pages to this topic in 1962 (in Capitalism and Freedom), four more in 1965 (in a National Review article), and four again in the New York Times [edit: David Gindis kindly points to me that he in fact wrote 2 other pieces in the early 1970s, one for a collective volume edited by Leonard Silk and another one for a bank journal. And he gave a few interviews]. In the 700-page memoir he penned with his wife and co-author, economist Rose Director Friedman, he allocated exactly two paragraphs to CSR, mentioning that he originally received $1,000 for the article and that “hardly a year goes by that we do not receive more than that for permission fees to reprint the article.” That’s roughly the same space Stanford historian Jennifer Burns devotes to the topic in her great recent intellectual biography of Friedman. Friedman’s massive archives at Stanford’s Hoover Institution contain just three folders on the subject—mostly correspondence with little-known businessmen between 1970 and 1994, yielding far less material than a single Newsweek column sometimes generated. Most of these folders contain data on corporate charities gathered by another researcher in the 1970s—a telling detail I’ll return to in the next post. So it seems “The Friedman Doctrine” quickly developed a life far more tremendous and independent from Friedman’s actual ideas about corporate social responsibility. But since it’s become an obligatory reference point—if not the starting point—for anyone interested in economists’ views on corporate purpose, and since it perfectly captures the shifting intellectual and political dynamics of its era, here are some thoughts on the piece, its meaning, contexts and legacy.

A ”stepping stone to socialism”

As Friedman himself noted, the 1970 NYT piece was essentially repeated arguments he’d made eight years earlier in Capitalism and Freedom. Indeed, he closed his piece by citing his own 1962 words: “there is one and only one social responsibility of business to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition, without deception or fraud.” His argument against CSR targeted recent instances where the government had asked business for self-restraint (like Kennedy’s anger over a price increase by US Steel) and what Friedman saw as a growing tendency among businessmen themselves to endorse the idea, for instance through charitable donations – “it prevents the individual stockholder from himself deciding how he should dispose of his funds.” Thes trends “undermine the very foundations of our free society,” he explained. Friedman had laid out his argument in a chapter otherwise devoted to monopoly, simply stating that monopoly’s existence, since it’s exempt from the discipline of competition “raises the issue of the “social responsibility’…of the monopolist.” Earlier in the book, he had explained that the rise of monopolistic situations didn’t merely result from businessmen’s behavior, but often stemmed from misguided public policies that granted monopoly power to large firms – not public monopoly itself but “the use of government to establish, support and enforce cartel and monopoly arrangements among private producers.”

Friedman returned to the topic in a 1965 National Review article that flagged CSR as a “subversive doctrine.” This time, his main target was President Johnson’s recent appeal to banks to show restraint in making loans to foreign borrowers to protect the balance of payment – itself reminiscent of previous calls to banks to restrict their credit to productive uses. His criticisms focused on the government’s silly move to request voluntary exercise of social responsibility from corporations rather than using coercive power (which he wouldn’t endorse either). In doing so, the government was dodging its responsibility and, at the same time, was unwilling to “let the price system work.” But Friedman also raised a new, more political argument: if businessmen (the “agents”) imposed sacrifices on the owners (the “principals”), they weren’t acting as businessmen but as “public servants”, despite not being selected “through an explicitly political process.” Thus CSR becomes a “stepping stone to socialism,” he concluded.

Both the context and content of Friedman’s final piece are well known, embedded in the New York Times column’s visuals featuring the main protagonists of “Campaign GM,” backed by lawyer and consumer advocate Ralph Nader. In an attempt to make General Motors more “responsible” regarding pollution, road safety, and quality, Nader’s group purchased twelve GM shares to attend the annual shareholder meeting. Among other reforms, they proposed establishing a shareholder committee for corporate social responsibility. In response, GM did appoint more diverse board members and began investing in social initiatives.

In his column, Friedman mentioned “the recent G.M. crusade” alongside many other examples he’d developed over the past decade. This time, the piece focused more thoroughly on the businessman or corporate executive than on government officials. As many have pointed out, Friedman wrongly claimed that executives are employed by shareholders and therefore should “conduct the business in accordance with their desires, which generally will be to make as much money as possible while conforming to the basic rules of the society.” This time, he also elaborated on the political implications of asking corporate executives to pursue social goals, reprising his argument that in doing so, businessmen effectively raise and spend taxes. They thus become “simultaneously legislator, executive and jurist… a public employee, a civil servant.” He added that “those who favor taxes and expenditures… have failed to persuade a majority of their fellow citizens to be of like mind and that they are seeking to attain by undemocratic procedures what they cannot attain by democratic procedures.” He included his usual warning that a “free society” (which he meant as one organized through the price system) makes it hard for good people to do good but also for evil people to do evil. “The political principle that underlies the market mechanism is unanimity,” he added, contrasting it with “conformity,” the political principle that in his view underlies the political mechanism. Without using an expression that he made much use of in his other writings, he was rejecting the tyranny of the majority. “There are no ‘social’ values, no ‘social’ responsibilities in any sense other than the shared values and responsibilities of individuals,” he concluded.

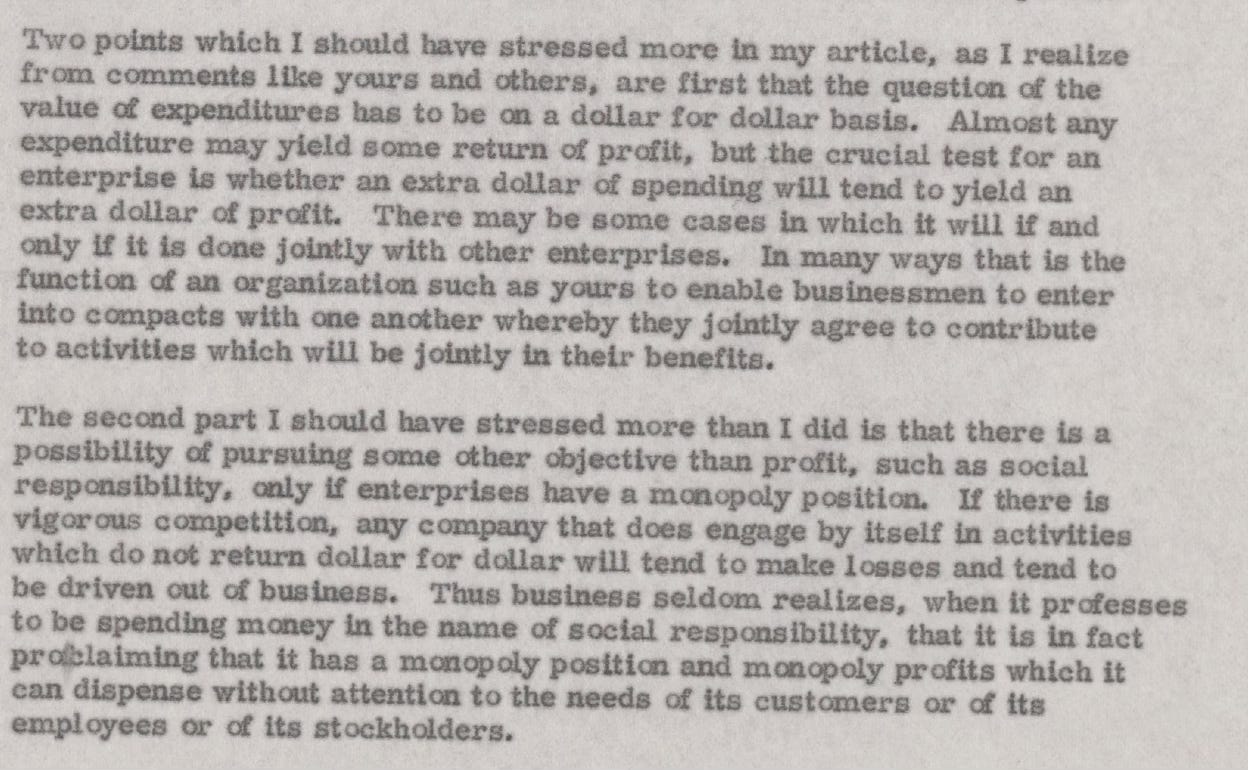

Among the many researchers who have surveyed Friedman’s evolving writing on CSR, historian David Chan Smith compellingly recapitulates the sources of his monopoly and political arguments. He places Friedman’s thinking in the context of rising big companies and monopolies, noting how scholars like Berle, Means, Dodd, and Bowen systematically observed that research questions about whom corporations should serve were inescapably tied to the growing size and market power of large corporations. CEOs themselves, from General Electric to Standard Oil and US Steel, were endorsing the CSR rationale. Chan Smith unpacks Friedman’s fears—not just of government regulation but of possible convergence between government and business interests. Government might create monopolies, but Friedman was increasingly concerned that businessmen would submit to what Chan Smith calls “internal politicization” (the corporation becomes a government agent) and that businessmen might use CSR as cover for regulatory capture (Friedman’s close friend and colleague George Stigler introduced the term in an article published the next year). Businessmen aren’t just “short-sighted and muddle-headed” but, in using the “cloak” of CSR, engage in “hypocritical window dressing,” even “fraud.” In a letter to the vice president of the National Association of Manufacturers a few weeks after the Timespublication, Friedman explained that he should have emphasized more that “when it professes to be spending money in the name of social responsibility, [business] is in fact proclaiming that it has a monopoly position.”

Friedman’s ambiguities are a feature, not a bug

The problem with interpreting the New York Times piece, though, is that Friedman proposed so many half-baked examples and lines of argument that you can rightfully pull any of the many sometimes inconsistent threads. This shows up prominently in the set of essays gathered on the ProMarket website for the 50th anniversary of Friedman’s Times piece. Chicago economist Luigi Zingales proposed turning the Friedman doctrine into a “Friedman Separation Theorem.” It states that under certain conditions—competitive environment, no externalities, complete contracts—it’s socially efficient for managers to maximize what has since become “shareholder value.” Since these conditions don’t hold, he argued (along with Olivier Hart), the appropriate objective function for a firm should be to maximize shareholder welfare. Finance professor Alex Edmans focused on the underlying lack of comparative advantage embedded in Friedman’s insistence that the value of expenditures must be measured “on a dollar for dollar basis.” Law professor Margaret Blair, among others, focused on the shaky legal foundations of Friedman’s piece.

An important aspect that scholars have overlooked is how much Friedman’s three CSR pieces (1962-1970) actually focus on macroeconomic stabilization rather than corporate governance per se. Friedman’s concern wasn’t just with attacks on the market system but with statecraft at large. And it derived as much from the concerns of the day as from Friedman’s longstanding research: if there’s a doctrine he was trying to sell in these years, it was monetarism. 1962 was the publication year of his and Anna Schwartz’s two decades of careful collection of money supply data and analysis, The Monetary History of the United States. He had published earlier with Stigler on price ceilings. His main Capitalism and Freedom example against CSR dealt with government exhortations that businesses “keep prices and wage rates down in order to avoid inflation.” His main 1965 target was Johnson’s message that banks should adapt their lending policies and, again, “the guideposts of the Council of Economic Advisors” on wages and prices. 1965 was the year British Conservative politician Iain Macleod coined the term “stagflation” during a speech to the House of Commons. The corporate executive “is told that he must contribute to fighting inflation,” Friedman complained in the 1970 piece, alongside denouncing a new call to fight “pollution,” a term Friedman returned to several times. His column appeared five months after the first Earth Day (April 1970), and just as environmental concerns were gaining momentum—two years before the OECD adopted the polluter-pays principle and economists began debating the Club of Rome report.

Overall, Friedman’s goal wasn’t so much to participate in a debate over corporate governance or what the firm’s goal should be. The 1970 piece was a combined set of arguments to protect free markets from various threats. It wasn’t meant as a theorem, not even a doctrine as the Times supertitle suggests. Furthermore, the many ambiguities in the Times piece aren’t a bug—they’re a feature. The think piece fought several evils at once (pressures, campaigns, and regulations on charities, pollution, macroeconomic stabilization, and more), weaving together ethical, legal, political, and efficiency arguments in a packed argument that Friedman never returned to. It wasn’t the first time he employed this strategy. Friedman’s only epistemology publication, “The Methodology of Positive Economics” (1953), was, by his later admission, framed with exactly the same strategy: it fought many evils at once (the Cowles Commission’s charge of “Measurement without Theory,” monopolistic competition, opponents to marginal cost pricing) with arguments that derived some of their huge appeal from their ambiguity (the “as if” methodology and the statement that a model’s success should be judged by its predictive rather than explanatory power). Yet Friedman never provided additional explanation or agreed to discuss it on purpose. Asked by historians and philosophers to respond to a series of comments for the 50th anniversary of the essay, he refused and explained: “I have myself added to the confusion by early adopting a policy of not replying to critiques of the articles… That act of self-denial has quite unintentionally been a plus for the discussion of methodology. It has left the field open for all comers.” Just like the Times piece, it shaped readers’ epistemological approach to models and realism for decades. And just like the Times piece’s title, it eventually evolved into a pop version (the “as if” statement) rather independent of the original writing. Both became slogans, magic formulas of their own that economists and commentators sought to use or condemn as weapons or curses (Expelliamus!)

From normative political stance to positive economic research on CSR

The comparison with the 1953 essay also highlights an important tension in Friedman’s writing on CSR and comments about it. The 1953 article concerns the methodology of positive economics. Friedman’s few CSR writings, however, are purely normative. These aren’t concerned with whether firms do maximize profits, but whether they should. And though normative economics was then a lively and prestigious field (with sharp ongoing battles over the definition of a welfare function by Arrow and Samuelson, Sen challenging the informational basis of ordinal utility functions, etc.), Friedman didn’t follow this line—he went straight into discussing the risks and benefits of alternative political structures. His pieces aren’t the product of a scientist but of a political thinker. As I have argued years ago, Friedman has always considered that the overall consistency of his political and scientific views on markets was a matter of “luck.” On monopolies, however, his “schizophrenia” created tensions. On the one hand, Friedman-the-political-thinker warned that large corporations endorsing CSR posed a threat to free society. On the other hand, Friedman-the-scientist constantly argued that the importance of monopolies in the US economy was greatly overestimated—in line with his own observations about the gap between the US and Europe, as well as empirical studies by Warren Nutter and other participants in Aaron Director’s Free Market Studies.

Moreover, the 1953 article was primarily written as a response to economists debating precisely whether they should write models assuming that firms maximize profit. The goal here isn’t to revisit what has been called the “marginal cost controversy” of the 1940s, which pitted proponents of monopolistic and imperfect competition against those advocating marginal cost hypotheses. Much has been written on this (see in particular Roger Backhouse’s article). My claim is that focusing too exclusively on Friedman’s piece has overshadowed the positive line of work that most economists were pursuing in these postwar decades on how to model firms’ behavior and goals. This history is partly theoretical, partly about tools as well. The 1940s controversy wasn’t just about hypotheses—it was also very much about using questionnaires to understand how businessmen set wages and prices and what goals they had in mind. The next post examines some of this research, from Baumol’s managerial theory of the firm to Arrow’s writings about CSR, early behavioral economists’ work, and how charitable giving shaped economists’ understanding of corporate goals.

Looking beyond the trigger

Before I get there, let me close this already too-long post with the question of Friedman’s legacy. Did his 1970 New York Times piece become an instant hit? Yes, of course—Friedman’s writing, just like Krugman’s today, has that power. Though there’s not yet a systematic bibliometric, network, and word-embedding study of its reception, a qualitative study of citations to his work up to the 1980s shows that it was immediately taken up in business and academic settings.

Was it instantly cited because it was new? No, it recapitulated an old line of thinking that Friedman himself attributed to no less than Adam Smith. Was it because it convinced people? Just the contrary. As Brian Cheffins explained, interpreting Friedman’s 1970 piece as launching the “shareholder primacy” movement gets both the post-Friedman chronology wrong and, as I will argue next, the pre-Friedman one too (shareholder/stakeholder are terms that Friedman never used). Cheffins, among other historians, argues that the business turn to shareholder primacy took place two decades later. Like many other CSR writers, he uses the statements of the Business Roundtable, a gathering of CEOs from major US companies. In 1981, their “statement on corporate responsibility” explained that “managers are expected to serve the public interest as well as private profit.” In 1990, the orientation still was “to carefully weigh the interests of all stakeholders as part of their responsibility to the corporation or to the long-term interests of its shareholders,” reflecting management research showing that the interests of shareholders and stakeholders were not only difficult to disentangle but also consistent with one another in the long term. The tone only changed in 1997: “the paramount duty of management and of boards of directors is to the corporation’s stockholders… the notion that the board must somehow balance the interest of other stakeholders fundamentally misconstrues the role of directors.” The next shift would occur in the 2019 statement, which began by stressing “a fundamental commitment to all of our stakeholders.”

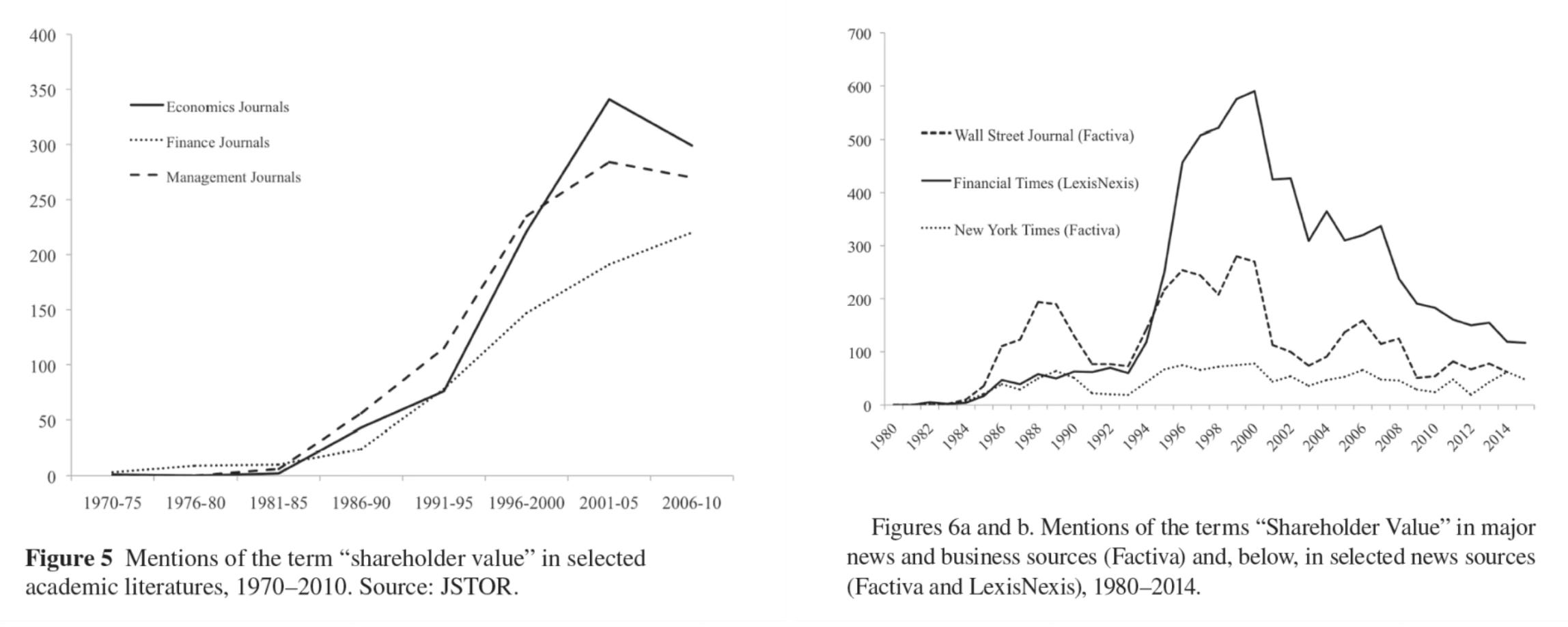

This is consistent with both quantitative and qualitative evidence offered by Marion Fourcade and Rakesh Khurana. They show that the notion of “shareholder value” strongly picks up both in academic publications and newspapers such as the Wall Street Journal, the Financial Times, and the New York Times beginning in the early 1990s—twenty years after Friedman’s piece.

To anticipate the next post, the chronology is thus: up to the 1930s, the default idea was that corporate executives should maximize profit. In 1931, lawyer and New Deal architect Adolf Berle (of Berle-Means separation-of-ownership-and-control fame) argued in the Harvard Law Reviewthat corporate powers should be used “only for the… benefit of all the shareholders as opposed to being left to director discretion.” He feared that with the growing size of US corporations, managers would become an oligarchy of their own. Law professor Merrick Dodd countered that it was “undesirable… to give increased emphasis at the present time to the view that business corporations exist for the sole purpose of making profits for their stockholders.” A debate ensued. By 1954, Berle conceded that “events and the corporate world pragmatically settled the argument in favor of Professor Dodd.” By the 1970s, most law, finance, and economics scholars were studying or arguing in favor of CSR. Nader and his Raiders dominated a public debate marked by business scandals, growing distrust toward giant corporations, and a flow of consumer and environmental regulations. The government was even considering using federal charters—the legal contract between corporations and the state—to redefine business-society relationships. To explore this possibility, Congress held hearings on Corporate Rights and Responsibilities in 1976.

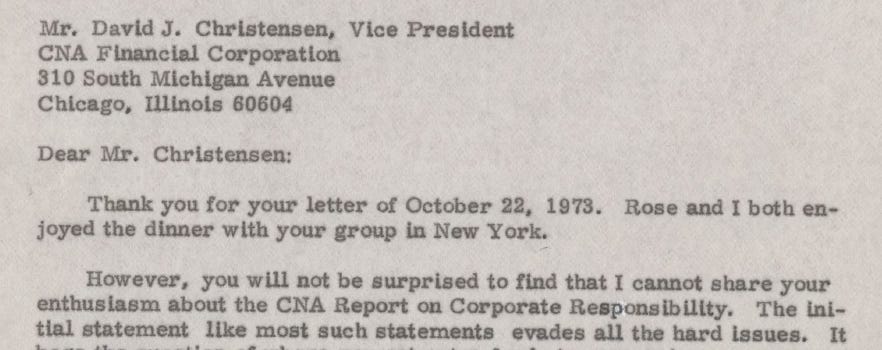

Why the tide turned in the 1980s is another topic. Cheffins points to the wave of corporate takeovers and new valuation methods in trading rooms. Fourcade and Khurana trace how Michael Jensen brought his ideas from Rochester to Harvard, where he established influential courses on corporate finance. But what is clear is that Friedman’s column was thus, as often, a resistance piece—one that didn’t change minds. The correspondence he received in response to the piece over the next decade was mostly from businessmen: the VP of the National Association of Manufacturers, the VP of CNA Financial Corporation, the PR director of Arthur D. Little. All of them disagreed with Friedman and offered rationales for why their firms should pursue social goals.

In 1998, Friedman reflected that the piece

“has become a standard item in business and law school courses on ethics. Teachers want to assign readings on ‘both sides.’ Few other economists have been willing to take so extreme (I would say, straightforward) a position, hence my article is in demand to present a defense of what most of the instructors doubtless regard as an indefensible position.”

As David Gindis demonstrated in an excellent article, the most vocal CSR critic was actually Henry Manne—a legal scholar who helped organize the law-and-economics movement—rather than Friedman. Manne spent most of the 1970s making largely unheeded arguments against corporate social responsibility. Friedman’s piece is important historically not because it not because it changed minds, but because it became a cultural touchstone. It was a “trigger”—and as Gindis reminds us, that was the term Jensen remembered Karl Brunner using when, a couple of years later, he asked Michael Jensen and Rochester colleague William Meckling to write a paper along Friedman’s lines. But that’s a story for a third post.

It’s a long week, itself nested in an endless stream of harrowing news. So here is a fun story of … More

Show full content

It’s a long week, itself nested in an endless stream of harrowing news. So here is a fun story of how new classical macroeconomics came to France. Of course, not just fun. This is a tiny story about the internationalization of US macro, but it’s part of the fabric of how economic ideas do travel, and it features interesting back and forth between theory and applied work, epistemology and policy/ideology. It also highlights the hopes of a young generation of intellectuals in troubled and uncertain times, one that led so many concerned scientists tried try to understand, harness and shape the “future.” As I research the 1970s and 1980s while teaching the ethos of this era to master and PhD students these weeks, I wonder what kind of hopes they are building for their scientific practices right now.

As any good 1980s French story, it involves postmodernism, art, fashion & nudes (and macro)

It’s 1981-1983 and two young French econ PhDs, Jacques Le Cacheux and Bernard Nivollet, are working as economists for the French Embassy in Washington. They are tasked with reporting on recent advances in economics US science. They quickly realize that seminar rooms and journals alike are abuzz with a new “new classical” style of writing theoretical models and taking them to data, in which expectations are rational, information is imperfect, but markets clear. The manifesto seems to be a 1978 article by Bob Lucas and Tom Sargent declaring large-scale macroeconometric modeling then used for policy guidance dead: “After Keynesian macroeconomics.”

So they decide to translate the paper in French and pen a companion review of the work and reactions generated by this approach in the next 5 years. Their title asked whether the “new classical school” is an epistemological revolution or a reactionary program. They carefully distinguished the approach from monetarismed, conclude that it is closer in method to game theory and, in a final sentence, explained that “despite the political consequences that were too quickly drawn from these works in the late 1970s…the scientific project that inspired them is…not conservative.

But they don’t submit the translation and associated survey to any of the main French academic journals, the Revue Economique, Les Cahiers d’Economie Politique or the Annales d’Economie et Statistique; they are young, they have no academic ambition, it’s 1983 so they agree to publish in a postmodernist journal recently founded by friends, Babylone. A pluridisciplinary group of intellectuals, the Babylone crew intends to create a conversation between art, architecture, sociology, economics, politics, poetry, philosophy and more. The issue is about understanding what is “post” in all this.

And Lucas-Sargent’s program was then definitely considered as as ‘post’ in economics as Teatro, Rivkin, Nouvel, Lyotard were ‘post’ in architecture and art The special issue also introduced another macro “post”-thinking, aka recent advances in French planning models for forecasting (prospective). Here is a quote from the volume’s introduction that summarizes the project, and how new classical macroeconomics fit in there.

“Post-modernists, post-Keynesians, post-sixty-eight! Babylon opens these variations around the post question. They will continue on postmodernism, and on the terrain of socialism, of real communism, and on that of the post-Yalta era in Europe with pacifism in upcoming issues. So are we neither neo-modernists, nor neo-Keynesians, no more than new philosophers or economists? We? or rather the situation that disappoints with evident pleasure the taxonomy for a French formal garden: Babylon is not precisely Versailles.”

And this is how, ladies and gentlemen, Lucas and Sargent came to France, in a volume on post-modernist architecture and macro, communism and pacifism, their attacks on Keynesian large macro-scale models intersected with architects’ sketches and pictures of topless women

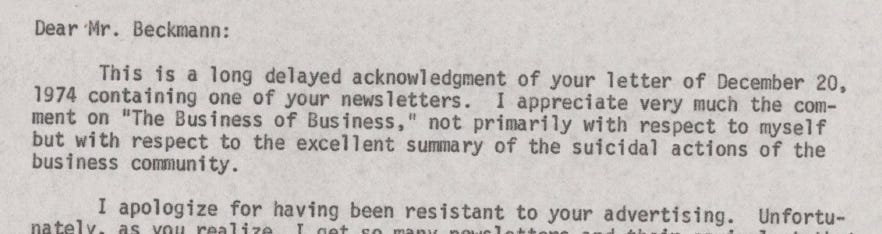

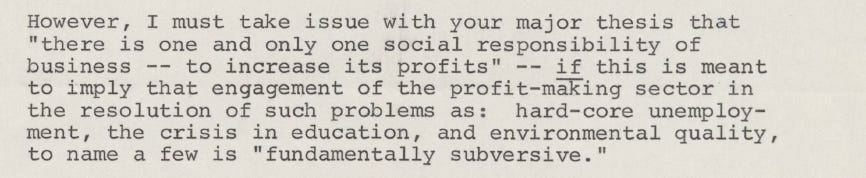

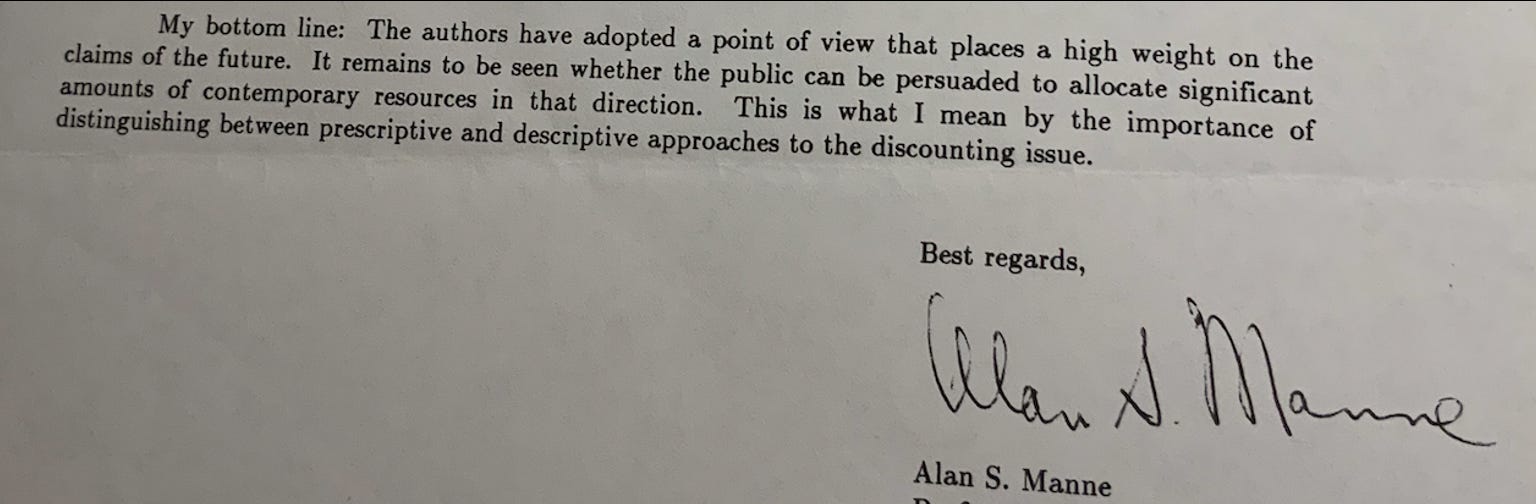

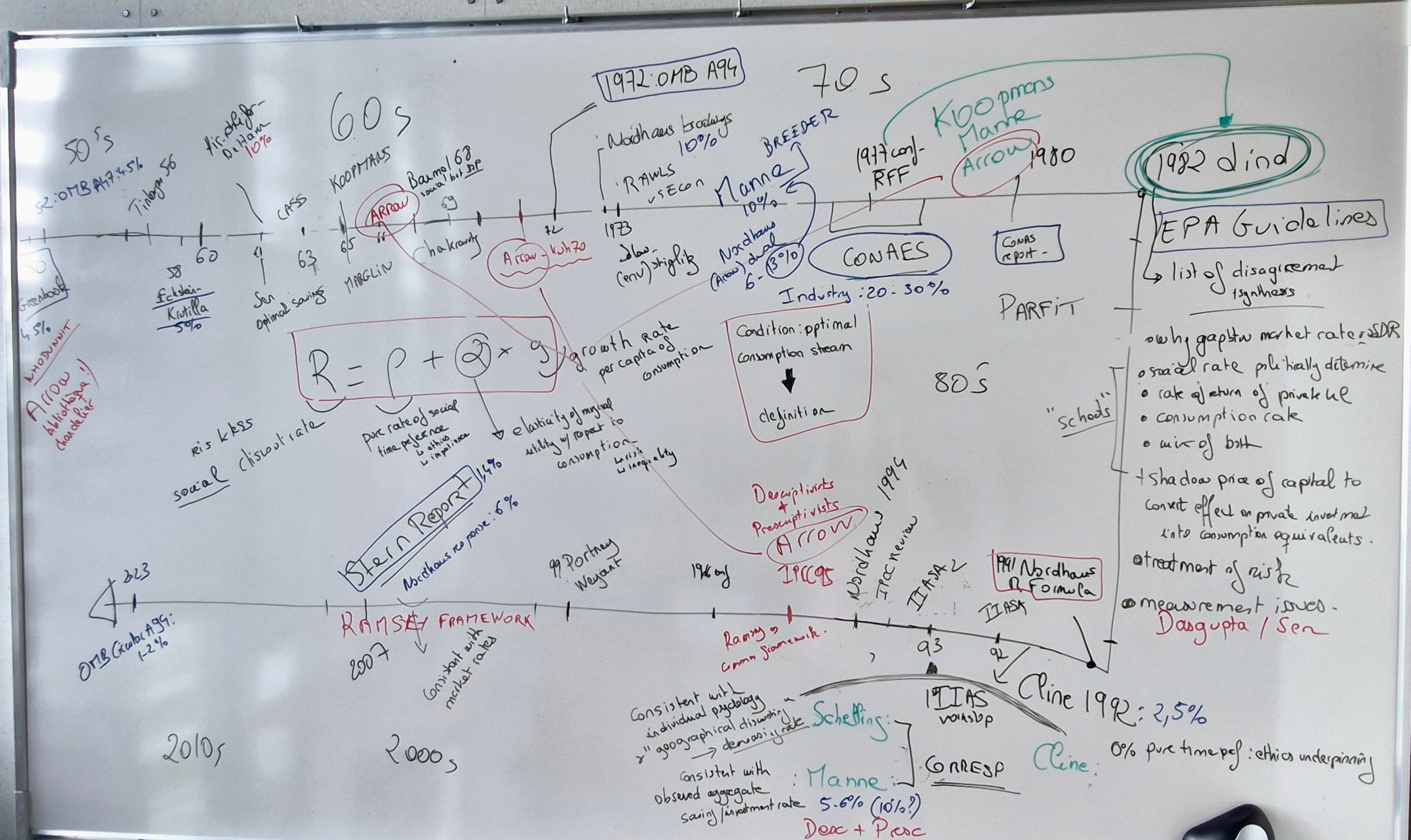

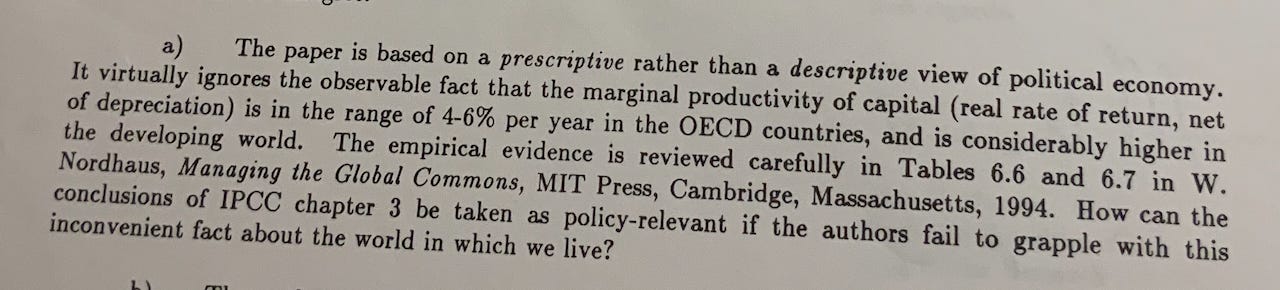

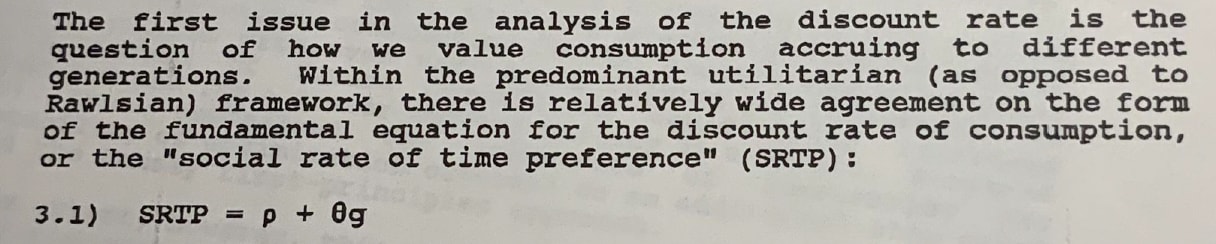

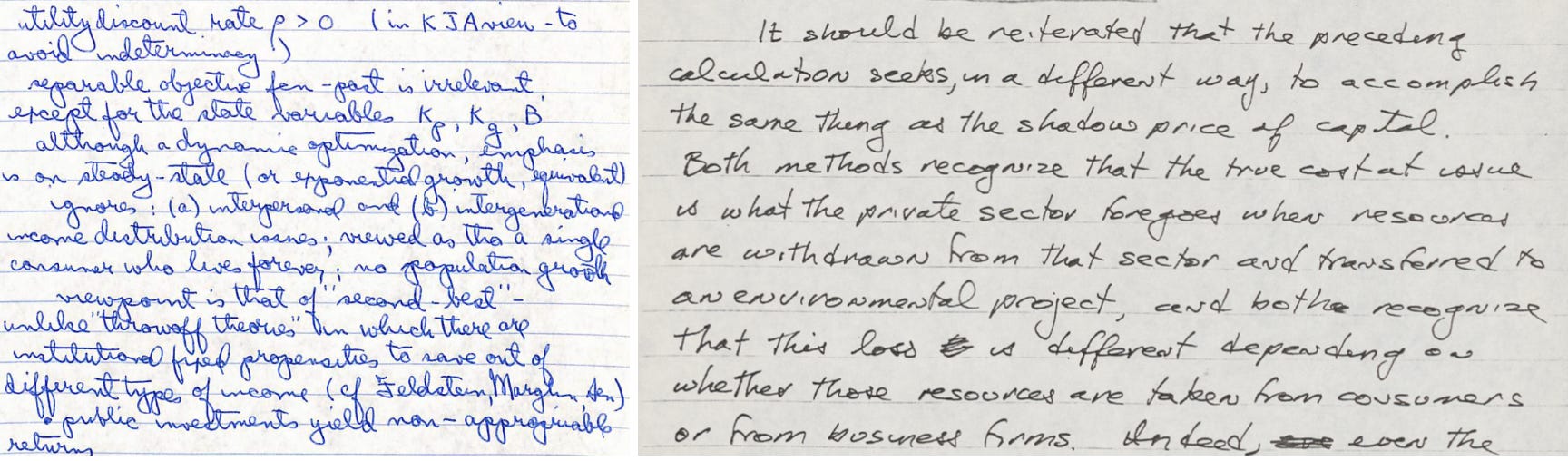

Alan Manne was the referee who suggested IPCC economists had taken a ‘prescriptivist’ view of discounting while he defended a ‘descriptivist’ one. Manne was already using the dichotomy during the IIASA 1993 workshop, and probably even before. One of the papers he presented at that workshop opened with a section titled “Time preference: prescription vs description.”

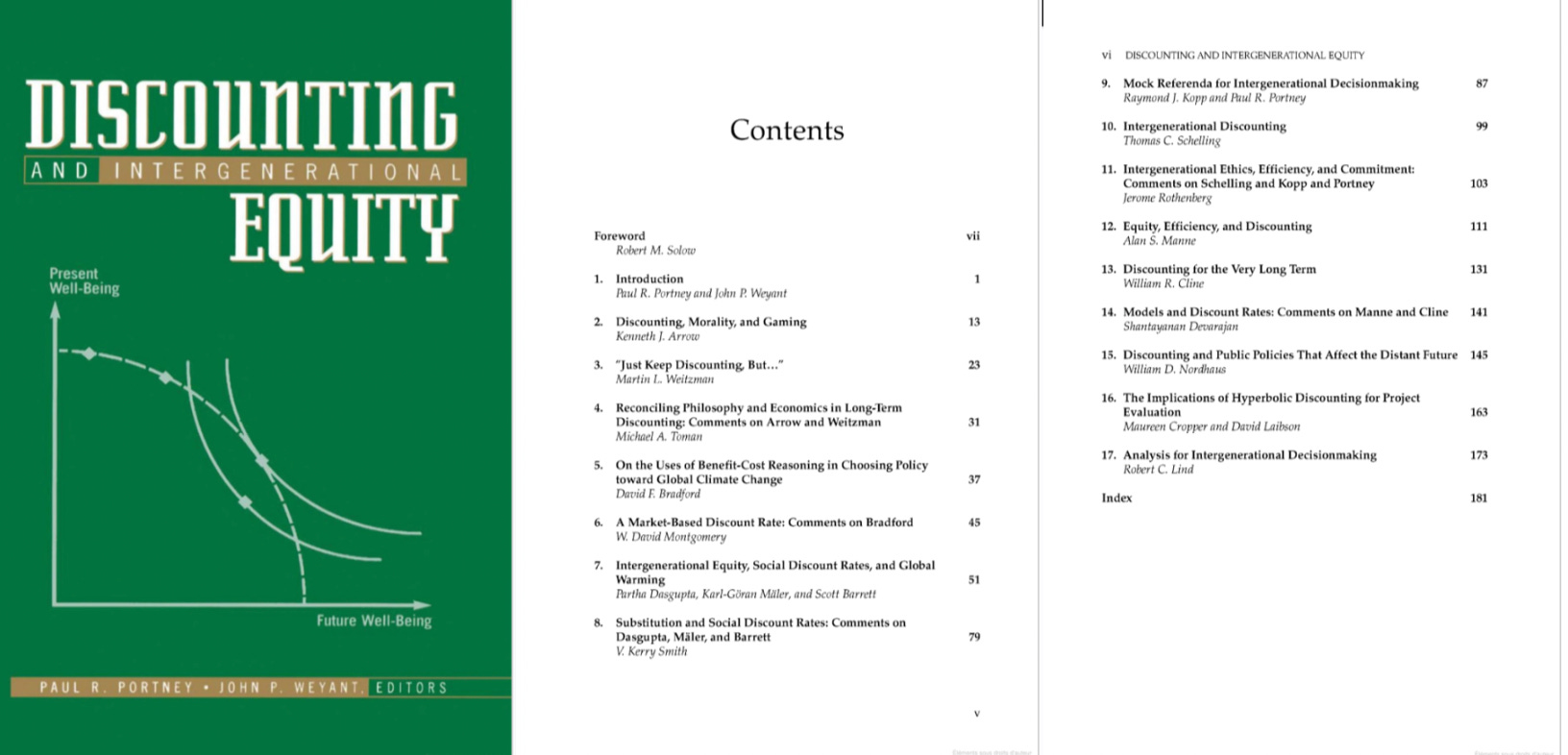

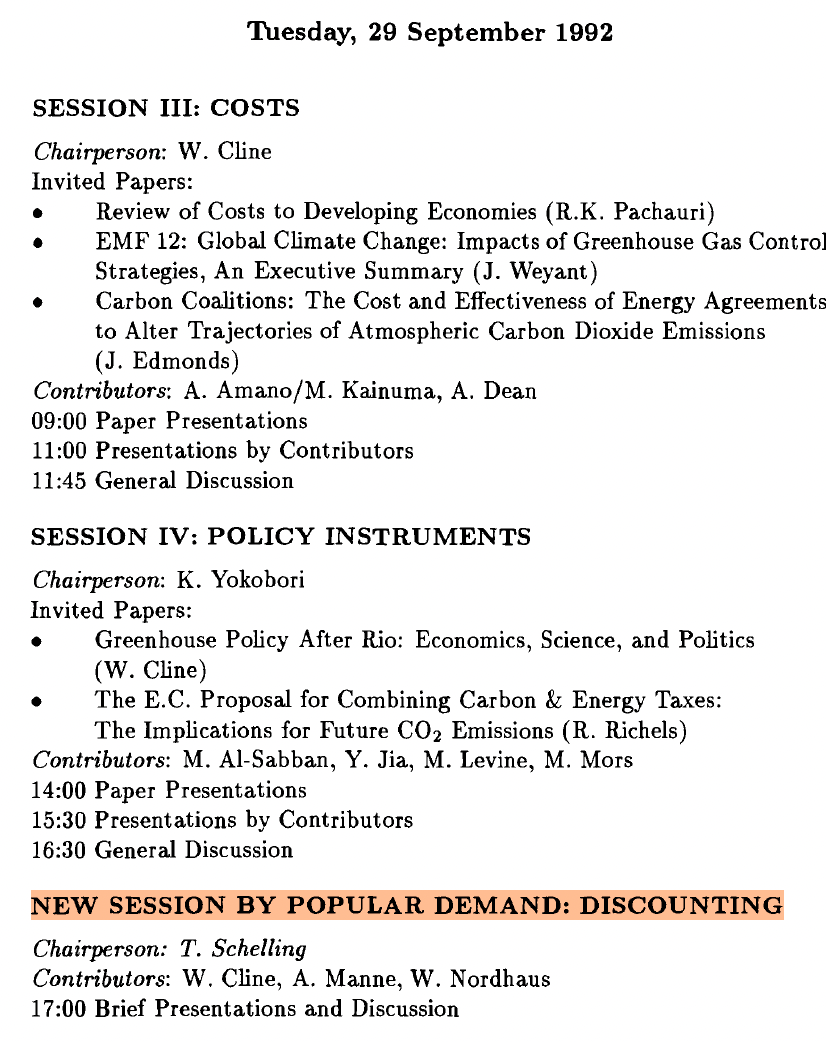

In the wake of the 1996 IPCC report, Paul Portney (the newly minted RFF president) and John Weyant (Energy Modeling Forum director and IPCC lead writer) put together a fresh conference on discounting. Both had participated in these debates since the 1970s. They circulated the IPCC chapter to potential attendees, noting that ‘in the mid-1990s, Lind’s apparent compromise seemed to unravel.’ Their questions probed how to handle projects with centuries-long impacts and whether discounting and cost-benefit analysis were really the right framework to tackle climate change or nuclear investments. The contributions were published in 1999.

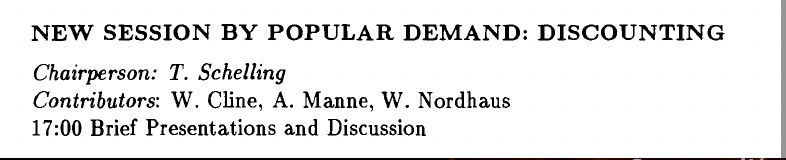

The conference was a mix of familiar faces and newcomers to the topic. Veterans included Schelling, Cline, Manne (whose paper again led with the prescriptive vs descriptive distinction before recasting discounting choices in terms of efficiency and equity), Nordhaus, Dasgupta, Goran-Mäler, and Arrow. True to form, Arrow penned the opening chapter. By this point, he’d delved deeper into ethics and contributed a piece on ‘morality’ and discounting.

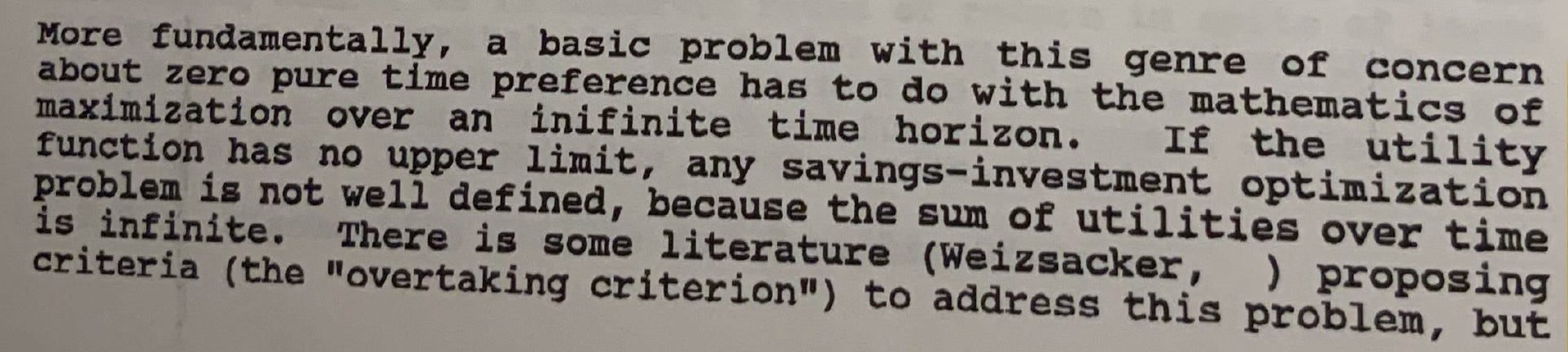

The contributions from newcomers highlighted how quickly the dynamics of the debates were shifting with the rise of climate modeling. While I’m still working out how to pin it down precisely, it seems the stabilization of the Ramsey equation (which participants recall was a hot topic during the conference) and the emergence of a rift between two approaches reopened Pandora’s box. Every parameter of the formula, as well as the framework from which it emerged, became subject to renewed scrutiny.

Maureen Cropper and David Laibson addressed the growing research on hyperbolic discounting that had gained momentum since Richard Thaler’s work. The concept of declining discount rates for decisions extending far into the future had been previously considered in Schelling-Manne-Nordhaus-Cline exchanges. However, the advancement of behavioral economics and laboratory reexaminations of individual time preferences provided a more structured approach to this line of inquiry. At the same time, new axiomaticfoundations for models involving indefinite futures or extinction were being developed.

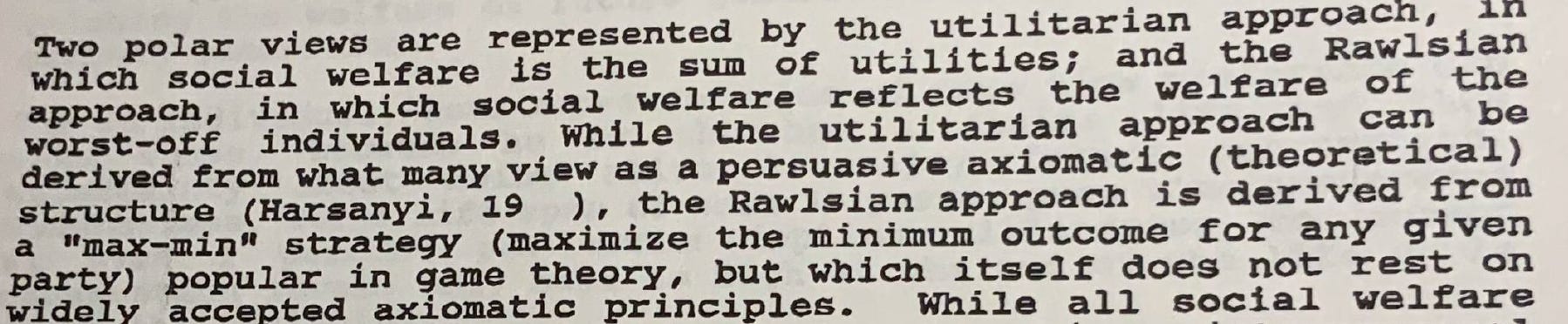

Lind’s proposition that the discount rate was not the appropriate mechanism to account for risk faced challenges. Martin Weitzman presented preliminary thoughts during the conference, anticipating later collective work on gamma discounting and risk-adjusted discounting. The paper by Portney and Kopp aligned with Schelling’s skepticism regarding the adequacy of discounting and its utilitarian underpinnings as a framework for addressing intergenerational justice. Adapting or challenging the utilitarian foundations on which discounting rests then developed into a flourishing area of research.

But these various lines of research constitute the present of discounting, which lies beyond our scope. They areaddressed in recentsurveys that appear regularly, often intertwined with many of the contributions covered in this series. So, you might wonder, what’s the point of digging into history when we could just read these surveys? While Pedro and I have fleshed out the narrative of the Ramsey Formula’s rise, we’re still mulling over the lessons to draw from it. Here are my tentative thoughts (for which Pedro bears no responsibility):

(1) Context is key: The discounting techniques and debates we’ve covered are rooted in a longstanding quest for a rational, scientific approach to public investment – first in the US, then worldwide. From the 1970s, it was paired with a specific focus with the distant or deep future. These techniques, debates, and the ebb and flow of concerns (like risk, intergenerational inequality, and axiomatic consistency) are also shaped by specific research questions: water investment in the 1950s, energy investment and evaluation investment in developing countries in the 1970s, and climate change from the 1990s onward.

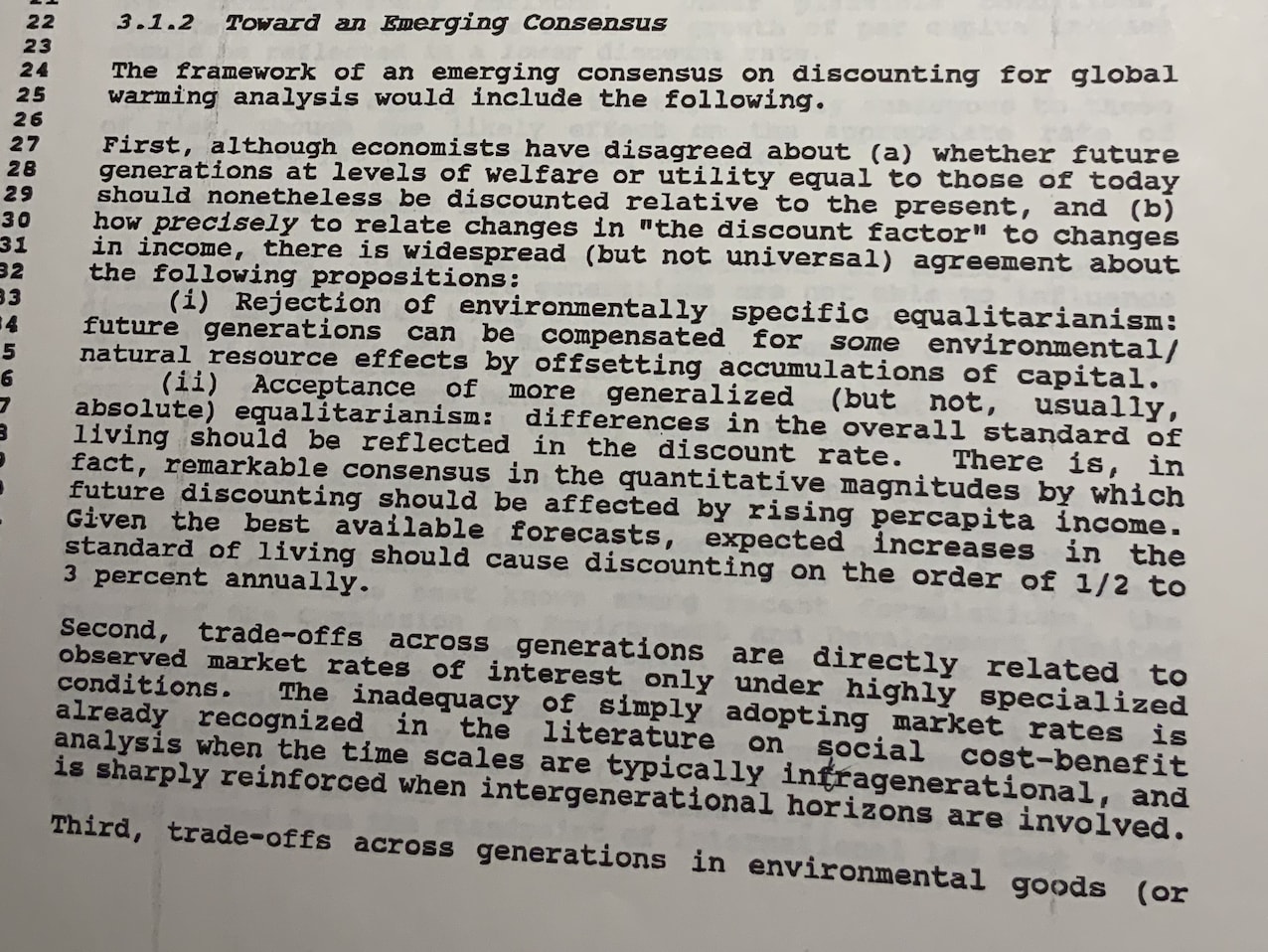

(2) This historical perspective I hope highlights how models, tools, concepts and categories develop and spread: think about Arrow’s pivotal role in disseminating the Ramsey formula, or Manne’s behind-the-scenes influence in framing disagreements about its application. It’s got me wondering: would economists today still identify as prescriptivists or descriptivists? Would they find these labels useful? The archives reveal that neither group is a united one. For instance, Nordhaus, Manne, and Schelling all advocate setting discount rates based on observed behavior – be it market data, macro time series, or behavioral surveys. But their justifications are different.

(3) The status of ambiguity in science: reading a survey on discounting often leaves one with a persistent sense of ambiguity. These are frequently structured as a menu of approaches to the problem of comparing present and future flows, and it’s not always clear how to relate them to one another or identify the sources of disagreements. The Ramsey formula isn’t immune to this ambiguity. Our research aims to unpack three sources for it:

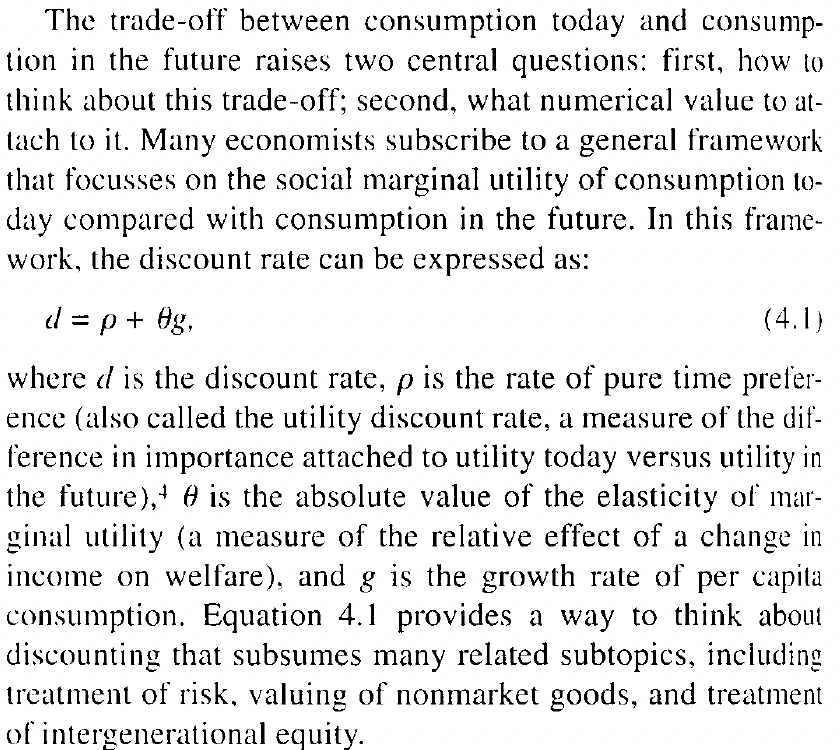

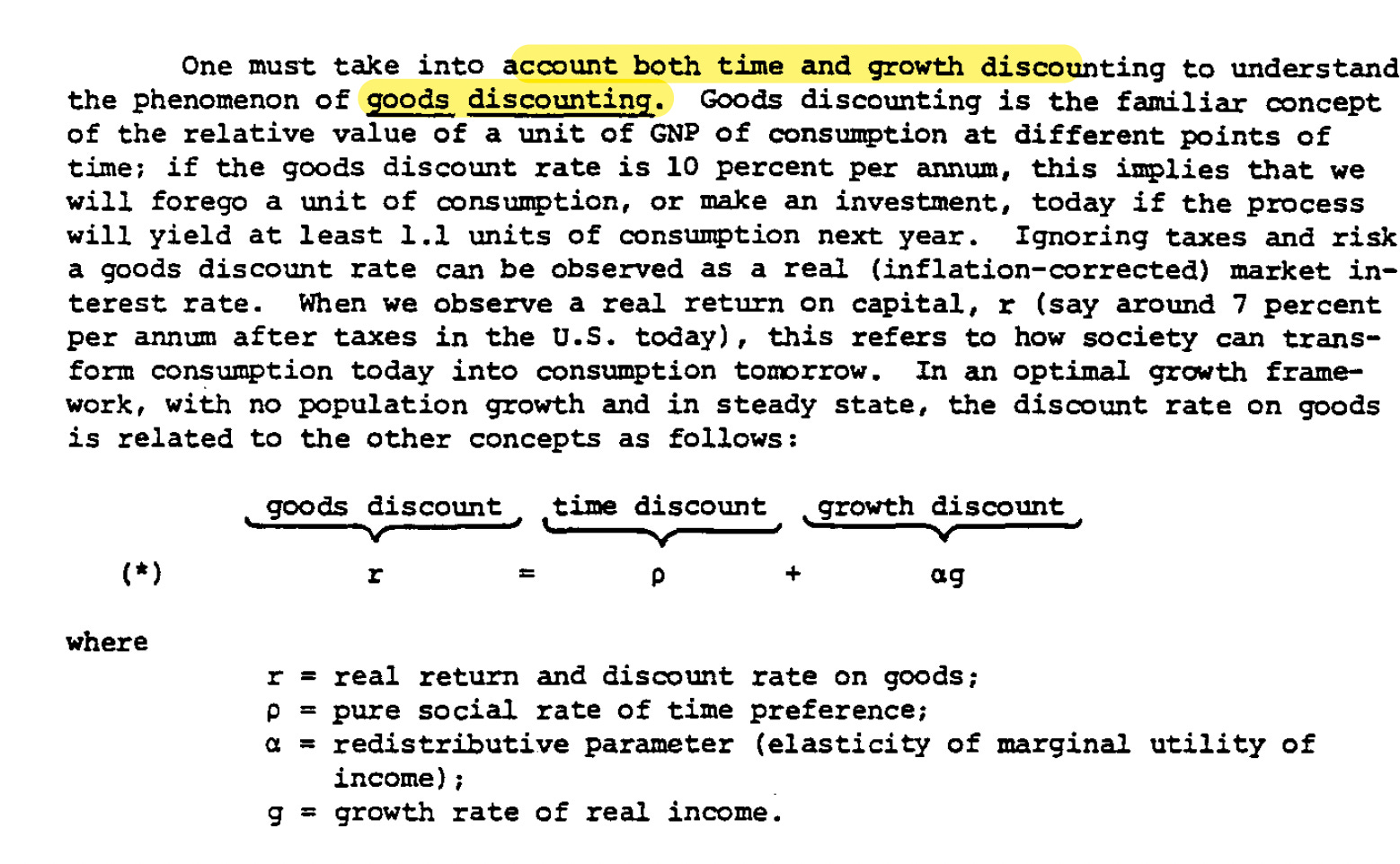

–First, there’s the ambiguity in the development of the Formula itself. When we talk about the “Ramsey formula,” we’re actually referring to two equations stemming from two frameworks. These are intertwined in Ramsey’s work and later theoretical work, particularly Arrow’s. The right-hand side of the equation is consistent, though the elasticity of marginal utility is sometimes interpreted as a risk aversion parameter, an inequality aversion parameter, or both. But the left-hand side is shrouded with ambiguity: when the equation is derived from the intertemporal utilitarian foundations Ramsey endorsed, it determines the social consumption rate or the social rate of time preference. But when it comes from the post-World War II optimal growth model, it’s an optimality condition determining the rate of return on investment in the steady state.

Philosopher Paul Kelleher, who has a forthcoming book on the social cost of carbon and discounting, makes a clear distinction between the “Ramsey formula” from intertemporal utilitarian analysis and the “Ramsey rule” from optimal growth models. But for most of the 20th century the terms were used interchangeably without clear distinction. This blurring of lines largely stems from the back-and-forth between frameworks, as we saw in our account of the IPCC chapter’s writing and revision (I’m still not sure which term to settle on – Ramsey formula or Ramsey equation).

–The second source of ambiguity relates to the formula’s travels from theoretical to applied economics, in particular cost-benefit analysis. The IPCC chapter, aiming at applications to climate modeling, is a prime example. Here, the Ramsey formula ultimately determines “the discount rate,” whatever is it. The focus has shifted from precise model-based derivations to parameterization. For some economists, it was an ethical decision about social time preference. For others, it was a consumption rate derived from agents’ behavior. Still others saw it as a calculated rate of return on investment, or simply a market rate.

–The third source of ambiguity arises from the constant juggling between theoretical and axiomatic consistency, ethical foundations, and tractability constraints in discounting discussions. While one aspect might take center stage in a particular work, the others are never far behind. And I hope this case study makes a strong argument for not dismissing tractability considerations in the history of economics. They need to be documented as carefully as other motives for choosing a model or tool. They’re persistent, and they’re shaping economists’ practices in significant ways.